.png)

Payment service providers (PSPs) are third-party companies that enable businesses to accept and process payments from customers across multiple payment methods.

As a merchant, they're the backbone of how you get paid, and the wrong choice can mean higher fees, limited payment methods, and a checkout experience that costs you conversions.

In this article, we'll cover the basics of a PSP and explore important considerations when selecting the right one for your business. We'll also explore how payment orchestration is changing the game for merchants, and why it might be the smartest upgrade to your payment stack.

Do you want to integrate with more PSPs without the hassle? Contact one of our payment experts to learn more.

What is a payment service provider (PSP)?

A PSP , sometimes called a merchant service provider, gives you the tools you need to accept payments from customers using credit cards, debit cards, or Alternative Payment Methods (APMs).

Simply put, a PSP’s main job is to ensure money moves safely and smoothly between buyers and sellers. It does this by offering a range of services, including a payment gateway, payment processing, and merchant accounts.

Are you new to payments? Check out our guide: A startup guide to selecting a Payment Service Provider

What services do payment service providers offer?

Processing payments involves various solutions at every step. Not long ago, you'd have needed to acquire the tools to facilitate each step in the payment lifecycle separately. That created a ton of complexity and was, more often than not, incredibly inefficient.

PSPs were created to simplify things by offering gateway, processing, and acquiring services in one package. That means you can handle an entire payment from start to finish with a single integration. Just think about Stripe’s promise of letting merchants accept credit card payments with just seven lines of code.

Over the last decade, as the payment processing ecosystem has become more complex, PSPs have added more services to give merchants more value. Here are some of the key services PSPs offer today:

- Payment processing: PSPs oversee the movement of funds from a customer's bank account to your account. They manage transaction authorization, clearing, and settlement.

- Payment gateway: A payment gateway facilitates the transfer of information between a customer and your acquiring bank.

- Fraud prevention: Fraud detection and prevention tools help safeguard transactions against fraudulent activities and illegitimate chargebacks.

- Currency conversion: Currency conversion services are crucial if you accept or make payments in multiple currencies. That said, most PSPs make FX decisions on your behalf by default, which can mean unnecessary conversions and costs you didn’t choose. More on how to solve that below.

- Reporting and analytics: Payment data is increasingly valuable for tracking and optimizing the payment process. PSPs typically provide transaction reports, financial analytics, and insights.

- Payouts and disbursements: Some PSPs offer payouts and disbursements, meaning you can send money to vendors, affiliates, or service providers without needing a separate tool.

How do PSPs process a payment?

The role of PSPs fits right into the bigger picture of online payment transactions. Let’s break it down step by step using an example:

- When your customer Jennie purchases a new watch online using her credit card, she enters her details at checkout and clicks 'pay.'

- The PSP's payment gateway captures this payment information and sends an authorization request to the PSP's acquiring engine. This request includes crucial transaction details such as card information, 3DS data, transaction initiation, recurring payment status, and network token usage.

- The acquiring engine then forwards this request to the card network (Visa or MasterCard) associated with the card used for the transaction.

- At this stage, the PSP steps back as the card network directs the information to the issuing bank, which assesses whether to approve or decline the payment.

- The card network communicates the issuer’s decision back to the PSP’s acquiring engine.

- If the payment is approved, a temporary hold is placed on Jennie’s account, showing that the funds are reserved and moving from her bank to your account.

- When you decide to finalize the payment, the PSP manages the funds transfer from Jennie’s bank to your account, and may handle reconciliation.

What are the benefits of using a payment service provider?

The primary advantage of using a PSP is that it consolidates most, if not all, essential payment services into a single package. That’s a shift from a decade ago when you’d have to set up separate integrations for different payment gateways and processors.

This streamlined approach not only simplifies things but also boosts performance. A PSP can enhance key performance indicators (KPIs) like transaction speed and reliability by handling the entire payment process from start to finish.

Beyond payment processing, PSPs extend their support into fraud management, reporting, reconciliation, and compliance, providing comprehensive solutions for your business.

How do you choose a payment service provider?

PSPs aren’t created equal. Each provider has strengths and weaknesses, whether that’s its range of solutions or its geographical reach. Choosing one that aligns with your business’s unique needs is crucial.

But with so many options, how should you decide which PSP to use? Let’s break it down.

- Work out your requirements: Start by listing out what you need. Consider both your must-haves and nice-to-haves. Think about the payment options you want to support, the regions you operate in, and any specific features important to your business.

- Research options: Identify potential PSPs and start narrowing down your choices by eliminating those that don’t meet your criteria. Tip: Don’t rely on online research. Ask your network for recommendations and check out industry reports.

- Compare fees: Once you have a shortlist, compare the setup fees, transaction fees, and any additional fees. Be mindful that different PSPs have varying processing fee structures. Tip: Decide whether you prefer a blended pricing model, which is more straightforward, or an IC++ pricing structure, which offers more detail and could help you improve your cashflow.

- Make your decision: Narrow your list and contact the providers. Ask for references from businesses like yours that have successfully used that PSP. You should have a clear winner.

Considerations when choosing a PSP

Every PSP is different, and the right one depends on your business model, markets, and growth plans. Here's what to look for:

- Payment methods: Verify if the PSP supports your customers’ preferred payment methods, including localized options. Assess how easy it is to add new payment types like digital wallets or Buy Now, Pay Later (BNPL).

- Security and compliance: Ensure compliance with industry standards like PCI DSS. Look for robust security measures covering encryption, fraud detection, and chargeback management.

- Global vs. local: If you operate internationally, choose a PSP with a global network of banks and financial institutions that can handle multi-currency transactions. But global reach alone isn’t enough. A PSP that works well in Europe may not support local payment methods your customers in APAC or the US expect. A PSP without local acquiring in your key markets can mean higher decline rates and unnecessary FX costs.

- Integration: Evaluate how easily the PSP can integrate with your existing ecommerce platform. Look for user-friendly APIs or plugins that streamline the setup process and minimize technical headaches.

- Customer support: Fast and efficient resolution of payment-related issues is vital to your revenue. Dedicated support matters, especially if your team has limited technical resources.

- Future-proofing: Consider whether the PSP can scale with your business. It should support future growth by adapting to new markets, emerging payment methods, and increasing transaction volumes.

- Reporting and analytics: Optimizing your payment systems can unlock revenue opportunities. Check what reporting tools and analytics you can access.

- User experience: Put yourself in your customers’ shoes. Does the PSP provide a user-friendly, seamless, and consistent payment experience?

- Redundancy and reliability: Downtime hurts revenue and damages customer trust. Verify the PSP’s redundancy measures and uptime guarantees to ensure your payment system is always available.

- Contract terms: Review the contract carefully, including the length of the agreement, monthly fees, and any termination fees.

- Compliance and legal considerations: Do your homework to ensure the PSP complies with legal requirements in your industry and region.

Why you should use more than one payment service provider

The era of relying solely on a single PSP for payment processing has ended.

Think about it: putting all your revenue eggs in one basket is risky. If your PSP experiences significant downtime, your entire revenue stream could come to a standstill overnight.

Even without that scenario, finding one PSP that meets all your service requirements across every market without any compromises is incredibly tough. And even if you do find one, how can you be sure they’re offering the best performance and pricing without any benchmarks for comparison?

That’s why top merchants are turning to a multi-PSP strategy. Using multiple PSPs lets you diversify your payment processing, reduce the risk of downtime, and optimize for better performance and cost. The challenge is that building a multi-PSP setup isn’t simple. It involves upfront development costs and ongoing maintenance that are resource-intensive and can slow your business down.

This is where payment orchestration comes in.

Payment orchestration is one of the hottest topics in payments. Our latest research finds that 87% of merchants are considering using orchestration in the next 12 months. Why? Because payment orchestration platforms let you scale your payment stack without complexity, using the services of multiple payment providers without spending the time and effort integrating with them directly.

.png)

Simplifying your payment stack by connecting with various PSPs is just the beginning. With payment orchestration, you gain the freedom and flexibility to execute your payment strategy quickly, turning payments into a powerful growth engine for your business.

Here are a few of the ways orchestration can help:

Optimize costs by managing all payment processors in one place

There are a few ways that using a payment orchestration platform can help you optimize costs:

- Having all your PSPs under one roof lets you compare performance more efficiently. You can use that data to negotiate more favorable contract rates based on actual performance.

- Unifying your payment stack eliminates the need for separate integrations, reducing initial development costs and ongoing maintenance associated with managing multiple PSP integrations.

- Payment orchestrators let you design tailored payment routes that direct online transactions to the most cost-effective provider based on region, payment method, or customer ID.

Taken together, this makes comparing performance, reducing integration costs, implementing smart routing strategies, and maintaining better control over your PSP relationships significantly easier.

Quickly expand to new markets by adding new payment methods with just a few clicks

Payment orchestrators come pre-connected with hundreds of PSPs and acquirers worldwide. Integrating with multiple PSPs, which would typically take months to build and maintain, can be completed in just days through a payment orchestrator.

Beyond simplifying PSP integrations, payment orchestrators make adding and managing local payment methods effortless. That’s crucial when expanding into new markets. Presenting the right payment methods at checkout based on your customer’s location boosts conversion and creates a more personalized experience.

Get a better understanding of your payments and optimize payment routes

Managing multiple PSPs often means juggling different portals to access your payment data. You’re logging into each PSP’s portal separately, exporting data, and trying to reconcile formats that don’t match. Each PSP reports differently and uses different standards, so you’re not always comparing apples with apples.

With a payment orchestrator, all your payment data is standardized and centralized in one dashboard. You can compare authorization rates across specific regions or acquirers, and understand which payment methods work best.

The best payment orchestrators let you go deeper into your data. You can analyze 3D Secure (3DS) performance across different markets or PSPs, and even drill down to the BIN level. This level of granularity helps you identify specific patterns, optimize conversion rates, and make informed decisions about when and where to implement 3DS for maximum impact.

You can then set up custom payment routes based on your findings. For example, if you discover that payments processed through Adyen in France have higher authorization rates, you can configure your orchestrator to automatically route all French transactions through Adyen. This strategic routing ensures that each payment is handled by the most effective PSP, enhancing both performance and cost efficiency.

As a payment team, a payment orchestrator allows you to deepen your understanding of your payments and create a strategy that is more aligned with your business goals.

A payment orchestrator acts like a control panel for all your payment needs, allowing you to:

- Boost authorization rates

- Optimize processing costs

- Recover more revenue

- Reduce payments fraud

- Uncover insights across your payment flows

- Scale globally without engineering overhead

- Minimize risk with global compliance

- Establish a test and learn mindset

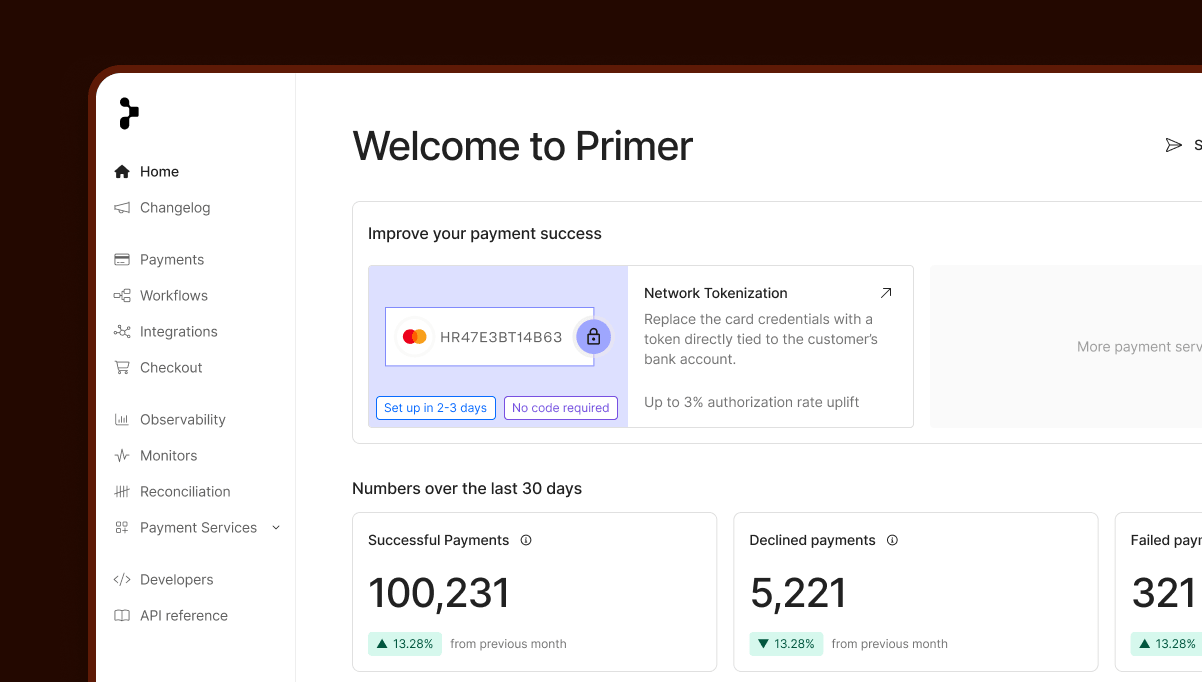

Why use Primer for your payment orchestration

Primer is a unified payment infrastructure. We help SMEs and large enterprises shape extraordinary customer experiences, process every payment with precision, and accelerate business growth without compromise.

Payment orchestration is just one of the powerful use cases we enable. With one integration to our platform, you can connect to as many PSPs as you need, access 100+ payment methods, set up custom payment flows, and track payment performance from a single dashboard.

Primer is built for ease of use. You don’t need a technical background to get started. Our no-code interface lets you manage your payment processes effortlessly, whether you’re setting up new payment methods or adjusting existing flows.

Here are a few key reasons merchants choose to work with new PSPs using Primer.

Integrate with new PSPs in days rather than months

We've already integrated with the world's leading PSPs and top local acquirers, so you can start using new PSPs in just a few clicks rather than months of development effort.

Enabling a new PSP with Primer is as simple as:

- Head to your Primer Dashboard

- Give Primer access to your processor account

- Choose which payment methods the processor should enable

%20(1).png)

For instance, when Australian gambling platform Dabble decided to launch in the US market, they initially faced a daunting option: set up direct integrations with US payment processors, which would have taken months. With Primer, they got there in days.

Read the full case study: Dabble picks a winner by partnering with Primer

Easily set up fallbacks to recover lost revenue

A fallback involves using a second processor if the first fails when completing a payment. Setting this up manually is highly complex since you need to understand retry logic and interpret the codes returned by each processor to know whether you can retry.

With Primer, you can use Workflows to set a trigger and select a fallback processor if a payment fails. We’ve also mapped and standardized decline codes across PSPs, so we automatically retry a payment based on the code and your chosen fallback processor. The result is higher authorization rates and a much better customer experience.

And because Primer 3DS is agnostic, your customers won’t have to go through another 3DS check on a retried payment.

.png)

Banxa recovered US$7 million in revenue with Primer Fallbacks in just six months, more than they initially suspected they were losing due to payment failures.

Introduce 3D Secure only when required

In Europe and a few other markets, 3DS is a requirement to complete a payment. While 3DS enhances security by adding an extra layer of authentication, it’s not required everywhere. In markets where 3DS isn’t mandatory, applying it can introduce unnecessary friction, leading to higher payment failures and lower conversion rates.

Primer is 3DS agnostic, meaning you're not locked into a single 3DS provider. Instead, you can connect the 3DS solution that works best for your business and use Primer to control exactly when authentication is triggered. This ensures 3DS is only activated when necessary, keeping friction low and conversion rates high.

.png)

Optimize your payments with network tokenization

We’ve integrated network tokenization into Primer to improve payment security and success rates across multiple PSPs.

Each token is uniquely tied to a specific merchant and customer combination, meaning that even if a token is intercepted, it can’t be used across different merchants. Network tokens have been shown to reduce fraud by as much as 26%.

Card details are also automatically updated, reducing the likelihood of failed transactions due to expired or outdated card information. This removes friction in the payment process and lets customers continue transactions without needing to re-enter their card details. Visa reports that businesses using network tokens see an average 4.6% uplift on approvals.

Read more: What are network tokens, and why should you use them?

Get a complete view of your payment analytics in a user-friendly way to help make data-driven decisions

Many orchestrators let you see your payment data in one place. At Primer, we’ve invested heavily in making our dashboards, monitors, and platform as intuitive as possible.

With Observability, you can see at a glance how all your PSPs are performing and slice the data in any way you need. Check authorization rates across the past 90 days for a specific processor. Analyze data based on decline reasons, MIDs, BIN numbers, and more.

You can interact fully with the charts and dig deeper into your data intuitively, hovering over a chart value to get a metric summary or clicking on a particular value to get a complete list of individual payments.

As Lucas Quinio, Head of Payments at Europe’s leading home furnishings retailer Conforama, puts it:

“Most payment solutions aren't very user-friendly. You need to have a deep understanding of payments to have any chance of using them. Primer breaks that mold. Everyone involved in the RFP commented on how intuitive the platform is and how they could see themselves becoming power users. That's incredibly important as we aim to allow everyone across the business to use payments to meet their goals.”

Take control of how you collect, convert, and move money

When it comes to global business, foreign exchange can be a drag. Most PSPs make FX and settlement decisions on your behalf. Funds get converted automatically at settlement, often without your input, at rates and timings you didn't choose. If you're operating across multiple markets, those hidden conversions add up fast.

Global Accounts changes that. It gives you local account infrastructure across markets so you can collect funds in local currencies, hold balances, and convert only when it makes sense for your business. Instead of your PSP deciding when and how your money moves, you do.

Settling in multiple currencies without unnecessary conversion at every step means lower FX costs and cleaner reconciliation. You can also use Global Accounts to hold balances across currencies and transfer funds globally, all within the same platform you use for accepting payments.

How AppsFlyer uses Primer to orchestrate payments and manage multiple PSPs

AppsFlyer is a SaaS leader in marketing measurement, attribution, and data analytics, with over 80,000 customers including Disney, TikTok, and SHEIN.

AppsFlyer initially worked with just one PSP but wanted to expand to multiple, giving it a more resilient payment strategy and a better payment experience for customers. After putting out a tender, AppsFlyer chose Primer. What set us apart? In the words of Senior Payments and Risk Project Manager, Shirly Katzir Kaslasy: usability and functionality.

After going live in January 2024, AppsFlyer can offer many more payment methods, has connected to more PSPs, experimented with different routing strategies, and used Fallbacks to increase authorization rates. Thanks to Primer’s no-code payment flows, they don't rely on the development team to make changes.

Learn more about AppsFlyer: AppsFlyer redefines the B2B payments experience with Primer.

Use a payment orchestration platform like Primer to manage your PSPs

By bringing multiple PSPs within a unified payment infrastructure provider like Primer, you can build a sophisticated payment stack without the development cost and complexity that typically comes with it.

Reach out to one of our payment experts to learn more about how Primer can help you.

.png)

Frequently Asked Questions (FAQs)

What is the difference between a payment service provider and a payment gateway?

A payment gateway is a technology that securely captures and transmits payment data from the customer to the acquiring bank. A payment service provider (PSP) typically includes a gateway as part of a broader offering that also covers payment processing, merchant accounts, fraud tools, and reporting. In other words, a gateway handles the data transfer, while a PSP provides the full infrastructure needed to accept and manage payments.

Can a business use more than one payment service provider?

Yes. Many merchants use multiple PSPs to improve reliability, expand payment method coverage, and optimize authorization rates. This strategy reduces the risk of downtime if one provider experiences issues and allows businesses to route payments to the PSP that performs best in a specific region or for a particular payment method. Payment orchestration platforms make managing multiple PSPs significantly easier by connecting them through a single integration.

How does payment orchestration help manage multiple PSPs?

Payment orchestration platforms act as a control layer that connects merchants to multiple PSPs, payment methods, and acquirers through a single integration. They centralize payment data, standardize reporting, and allow merchants to create routing rules that direct transactions to the most effective provider. This helps businesses optimize authorization rates, reduce costs, and expand into new markets without building and maintaining separate integrations for each PSP.

.png)

.avif)