What is card payment tokenization, and why does it matter for merchants?

Tokenization is the process of replacing sensitive card data with secure tokens that hold no value if stolen.

While it’s often treated as a security feature, it also plays a structural role in how flexible or constrained your payment stack will be as you scale. Done right, it reduces fraud and improves authorization rates. Done wrong, it locks you into providers and creates operational debt.

In this guide, we’ll focus specifically on card tokenization at the merchant and processor level: what it is, how it benefits merchants, and how to unlock its full value without sacrificing flexibility.

Primer is a unified payments infrastructure platform that empowers merchants to implement tokenization without lock-in and technical complexity. Book a call with Primer to learn more about how we can help.

What is card payment tokenization, and how does it work?

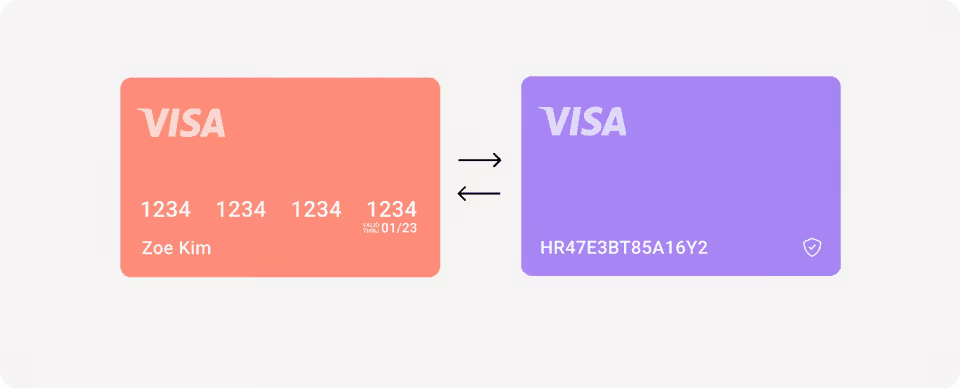

Card tokenization is a security method that replaces sensitive card data, most commonly the 16-digit PAN (Primary Account Number), with a unique, randomly generated token.

The token can’t be decrypted or reverse-engineered to recover the original card number. On its own, it also can’t be used to make a payment. Tokens are authenticated against the secure vault and the specific merchant or payment context in which they were created.

Think of them like an arcade chip that only works inside a single arcade and only when the machine recognizes it. If someone steals the chip and takes it elsewhere, it has no value and can’t be used to play.

Because the real card data remains locked inside a PCI-compliant vault, merchants never store or process raw PANs. Instead, they store the token and use it for subscriptions, one-click checkouts, refunds, and other payment flows without exposing sensitive card information.

Behind the scenes, the actual card information is securely stored in a PCI-compliant vault separate from the merchant’s systems (usually at the payment service provider or payment orchestration platform). Rather than store the raw PAN, the merchant keeps the token on file and uses it for subscription renewals, one-click checkouts, or refunds.

As a result, merchants face a lower risk of breach and fraud while ensuring compliance with the PCI DSS.

A step-by-step example of how tokenization works

- During checkout, the customer types in their card details.

- The 16-digit PAN is submitted directly to the payment processor or orchestration platform.

- The payment service provider (PSP) or orchestration platform validates the PAN, stores it in a secure vault, and generates a token. Tokens can be single-use (for one transaction) or multi-use (for recurring payments or stored customer profiles).

- The token is returned to and stored in the merchant’s systems.

- The merchant sends the token and transaction details to its payment gateway or PSP to authorize transactions.

- The PSP or token vault provider internally maps the token back to the real PAN, formats an authorization request, and forwards it to the issuer (the customer’s bank) through the card network (like Visa or Mastercard).

- The issuer approves or declines the request based on account balance, fraud rules, SCA, and other factors.

- The merchant only ever sees whether the transaction has been approved or declined, as well as the token reference.

Key benefits of card tokenization

Over half of merchants now use tokenization to:

1. Reduce fraud and protect customer data

Juniper Research projects that ecommerce fraud will jump from $44.3B in 2024 to $107B by 2029. For merchants, this means additional compliance burden, more chargebacks, and real financial loss, such as absorbing the cost of goods shipped to fraudsters.

Payment tokenization can help in the battle against fraud by replacing real card data with tokens that can’t be reverse-engineered. In the event of a breach, fraudsters are left with useless information, and the compromised data poses no risk to customers.

Network tokenization is particularly powerful against fraud: for example, it helps with the elimination of replay attacks thanks to transaction-specific codes called ‘dynamic cryptograms’. In fact, Visa has reported that network tokenization alone has driven a 30% reduction in fraud online.

2. Streamline PCI DSS compliance

Tokenization significantly reduces the compliance burden for merchants.

Without it, every system that stores or transmits card data falls within PCI DSS scope. This means merchants must encrypt databases, segment networks, restrict and monitor access, and complete complex, often costly audits.

With tokenization, sensitive card data never touches the merchant’s systems. Tokens aren’t considered cardholder data under PCI DSS, so the compliance scope shrinks dramatically.

In practice, that means:

- Fewer systems and servers to secure

- Less need for encryption and network segmentation

- Simpler, less frequent PCI audits

By removing sensitive data from the merchant environment, tokenization helps reduce risk, simplify compliance, and lower the ongoing cost of maintaining PCI DSS standards.

3. Boost authorization rates and reduce churn

Tokenization doesn’t just make payments more secure, it can also increase authorization rates and drive merchant revenue.

This is because card networks see tokenized transactions as lower risk, resulting in fewer false declines.

4. Simplify the checkout experience

In our 2023 study on the state of ecommerce in the UK, we found that 76% of shoppers abandoned carts due to a slow payment process.

Tokenization removes a lot of friction at checkout, making it easier for customers to complete purchases.

It helps with:

- One-click checkouts: Tokens enable saved card functionality, which means customers can shop without re-entering their card details. Raw PANs remain hidden throughout the process.

- Recurring payments: With tokens, merchants don’t need to ask customers to re-enter payment information when it comes to automatic billing for memberships or recurring orders.

- Omnichannel payments: Tokenization can be used online, in-app, or in-store, offering customers a more seamless experience at all points of sale.

Customers get to enjoy fast and convenient payments under high security standards, and merchants stand to benefit from increased sales.

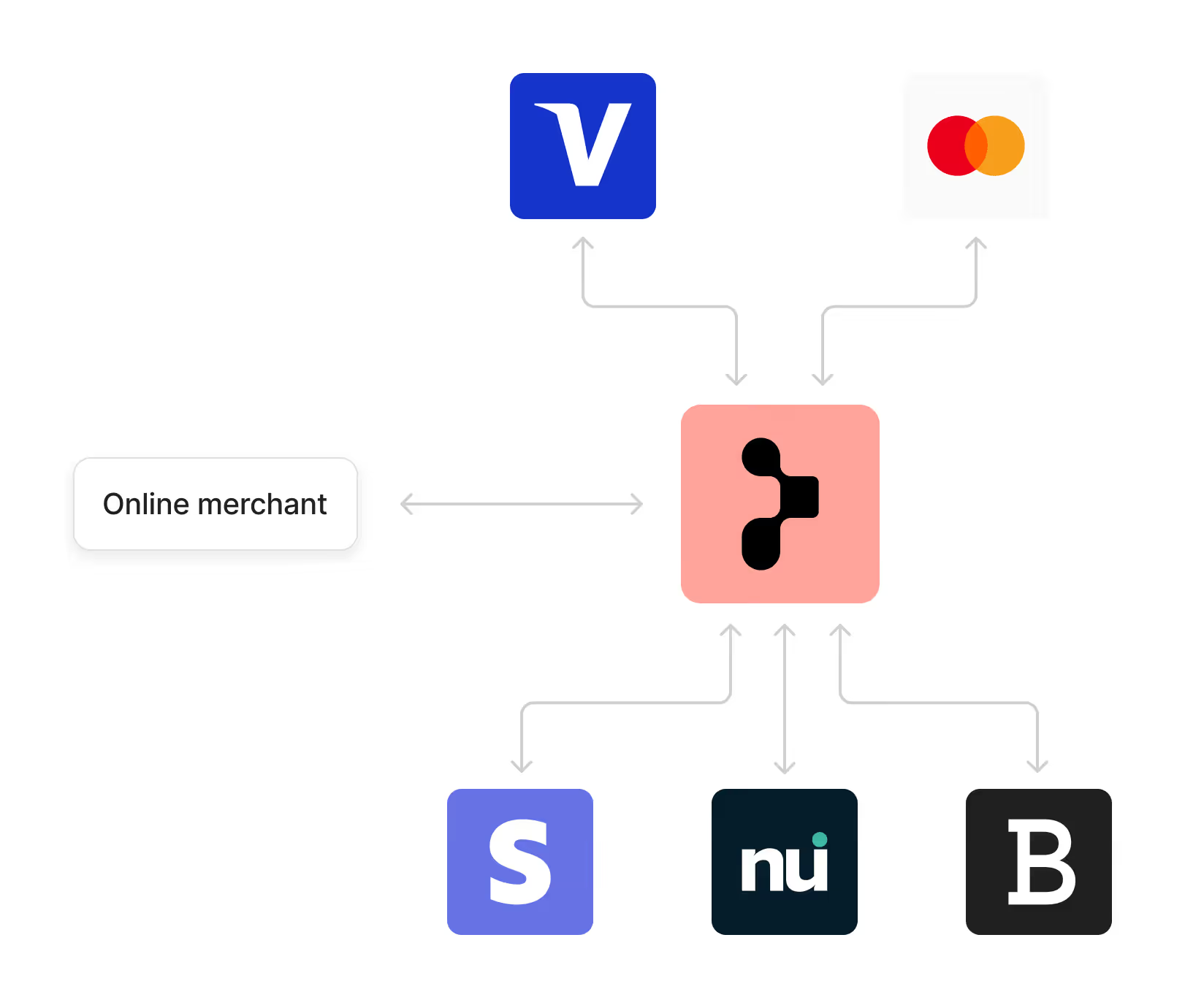

The challenge of managing payment tokens across multiple providers

For merchants operating across regions or using multiple PSPs, token management can quickly become a hidden source of complexity.

Most tokens are issued and stored within a processor’s own vault, which means they can’t easily move between providers.

At first, this may not seem like a problem… until you need to route transactions differently, expand into new markets, or add redundancy to your payment stack.

At that point, tokens tied to one PSP become technical debt. Merchants often have to duplicate customer vaults, re-collect payment details, and rebuild token logic for each provider. The operational overhead grows, and customers can experience failed payments or checkout friction when their stored cards no longer work.

Staying with a single PSP avoids the migration issue but creates another risk: dependency. A provider outage, integration change, or regional limitation can suddenly put a stop to thousands of transactions.

That’s why leading merchants are now shifting toward unified tokenization: a model that decouples token management from individual processors and keeps customer payment data portable across the entire payment stack.

How Primer helps merchants implement tokenization across multiple PSPs

Primer was built to turn payments from an operational burden into a growth driver.

Most merchants store tokens with their payment processor. That’s fine until you add another PSP. Suddenly, your tokens no longer work across systems, and you’re stuck either rebuilding your customer vault or staying locked in with one provider.

As a unified payments infrastructure platform, Primer enables you to manage tokenization once and use it everywhere.

Primer acts as a secure layer between your business and your processors. Customer card data is stored in a PCI-DSS Level 1 vault, and you receive Primer Vault tokens that work across all PSPs.

Behind the scenes, Primer handles the mapping, routing, and processing logic so your team doesn’t have to.

If you add or switch processors, your tokens stay the same. Customers don’t need to re-enter card details, and you avoid failed transactions or migrations.

In short:

- No complex integrations

- No vendor lock-in

- No friction for your customers

Support for network tokenization, without the integration burden

In addition to managing processor-issued tokens across PSPs, Primer also supports network tokenization. Network tokens are card-network–issued tokens, provided by schemes like Visa and Mastercard, that replace the PAN at the network level rather than inside a single processor’s vault.

Because they’re managed by the card networks, these tokens can automatically update when a card is reissued or expires, which helps reduce declines and improve authorization rates for saved cards and recurring payments.

Primer handles the technical setup, provisioning, and ongoing updates behind the scenes, so you can benefit from network tokens while still managing all of your payment flows through a single, unified layer.

If you’d like to go deeper into how network tokens work and when to use them, you can read our full guide here: How to optimize payments using network tokenization

Use Primer to easily unify tokenization across providers

Tokenization is more than a security measure. It’s a way to cut costs, improve the customer experience, and simplify compliance.

With Primer, you get the benefits of PCI and network tokenization without the extra complexity. No multiple integrations, no provider lock-in. Just a single, unified vault that powers secure payments across all your processors.

Want to learn more about how we can help you? Book a call with our team.

FAQs: Card tokenization

1. What is card tokenization?

Card tokenization replaces sensitive card details with unique tokens that hold no value if stolen. The real card data is securely stored in a PCI-compliant vault at the payment processor or payment orchestration platform, while merchants use tokens to process payments safely.

2. How does tokenization benefit merchants?

Tokenization reduces the risk of fraud and data breaches, simplifies PCI DSS compliance, increases authorization rates, and enables smoother customer experiences like one-click checkouts or recurring payments.

3. What’s the difference between card tokenization and network tokenization?

While tokenization is an umbrella term for replacing sensitive card data with secure tokens, network tokenization is a specific type of tokenization managed by card networks like Visa or Mastercard.

Payment tokens are usually issued by processors and tied to a specific provider. Network tokens, on the other hand, are issued by the networks, and they automatically update when cards are reissued. They also often achieve higher authorization rates.

4. How is tokenization different from encryption?

Encryption protects data in transit and at rest by converting it into unreadable code that can be decrypted with a key. Tokenization replaces the data entirely with a non-sensitive token, removing real card information from merchant systems completely. Together, they form a stronger defense layer against fraudsters.

5. Is card tokenization difficult to set up?

Setting it up on your own can be difficult. You must either manage multiple integrations across different PSPs and rebuild your customer vault each time you add a new processor, or risk vendor lock-in.

With a unified payments infrastructure platform like Primer, tokenization is built in and easy to set up. This means you can securely handle PCI and network tokens across all processors without added engineering complexity.

.png)