Agentic commerce is no longer just a thought experiment.

In a limited scope, AI agents are already starting to reshape how customers discover products, compare options, and in some cases, complete purchases, with or without a human ever visiting a merchant's site.

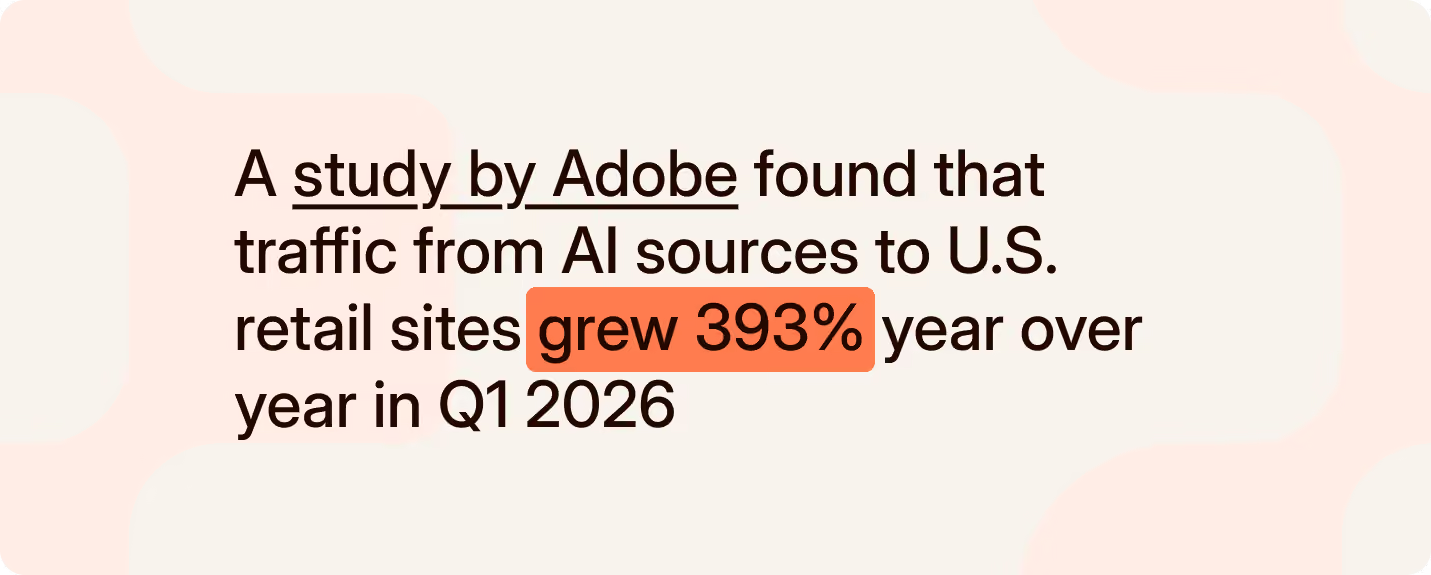

And the growth will come. Morgan Stanley estimates that AI shopping assistants could influence between $190 billion and $385 billion of US ecommerce spend by 2030, while McKinsey predicts that agentic commerce could orchestrate $3 trillion to $5 trillion in global revenue by the end of the decade.

The payment industry has never moved in lockstep. Agentic commerce is arriving the same way: fragmented, fast, and with every major platform pushing its own model. And merchants are being asked to make decisions before the rules exist.

Which is exactly why every payment leader is asking the same question: what should we actually do, and when?

This article will explain what agentic commerce is, how it could reshape checkout, and why the current protocol landscape makes picking a side challenging.

Primer is an AI-native Unified Payment Infrastructure that helps merchants connect and manage all of their payment services in one place.

What is agentic commerce?

Agentic commerce has become a catch-all term for AI-powered shopping. The problem is that it lumps together two related but ultimately distinct concepts: agent-assisted and agent-led commerce.

Here’s how they differ:

- Agent-assisted commerce is when a shopping assistant, chatbot, or AI tool helps a customer discover products, compare options, or build a basket through a natural language interface. The customer is still handed off to the merchant's checkout to complete the purchase.

Example: A customer asks an AI assistant to find a running shoe under $120 for marathon training. The assistant compares options, recommends a pair, and sends the customer to the merchant's site to complete checkout.

This is already happening at scale: according to Salesforce data, 39% of consumers, and more than half of Gen Z, already use AI for product discovery.

- Agent-led commerce is where the AI agent doesn’t just help the customer choose what to buy; it helps initiate or complete purchases on their behalf using a delegated payment token, stored credential, wallet, or emerging agentic commerce protocol.

Example: A customer asks an AI agent to find return flights from London to New York for a specific weekend and book them if the price drops below $450. The agent monitors available fares, checks the customer’s preferences around airline, baggage, timings, and cancellation policy, then initiates the booking using an approved payment method once the conditions are met.

The benefits of agentic commerce for merchants

Both agent-assisted and agent-led commerce could create meaningful opportunities for merchants. The benefits differ depending on how much of the journey the agent controls.

With agent-assisted commerce, the main benefits lie in discovery. As customers begin using AI agents to research products, compare options, and narrow down choices, more buying decisions could be shaped before the customer reaches a merchant’s website. That creates a new discovery layer between the customer and the merchant.

For merchants, this could create opportunities to:

- Reach higher-intent customers earlier: A customer asking an agent to compare options, check availability, or recommend the best fit is usually further along than someone passively browsing. The merchant has a chance to enter the shortlist while the customer is still deciding what to buy and where to buy it.

- Win customers who might not find them through traditional channels: Agent-assisted commerce could give merchants a new route into the customer’s consideration set. In traditional discovery, shoppers often find merchants through search rankings, ads, marketplaces, or brands they already know.

But agents can recommend options based on the customer’s specific needs, not just who ranks highest or spends the most on ads. That means a merchant with the most relevant product, price, availability, delivery option, or returns policy could be recommended even if the customer had not searched for that merchant directly.

The trade-off is that merchants may have less influence over how their products are discovered, compared, and presented. If the agent controls the research journey, the merchant may not know which options the customer saw, what criteria shaped the recommendation, or which messages, reviews, policies, or competitors influenced the final decision.

Discovery is where merchants build trust, show why they’re different, and learn what customers care about before checkout. If that moves into an agent-controlled interface, merchants may gain reach, but lose visibility, brand control, and customer insight.

Agent-led commerce goes a step further.

Instead of only helping the customer decide what to buy, the agent can also act on that decision. If the customer gives the agent permission to purchase within certain rules, the merchant has an opportunity to remove more of the friction that usually sits between intent and checkout.

With agent-led commerce, merchants can:

- Eliminate the gap between intent and purchase: Cart abandonment remains one of ecommerce’s biggest structural leaks, with Baymard’s 2026 benchmark putting the average cart abandonment rate at roughly 70%.

Agent-led commerce could reduce cart abandonment because there are fewer friction points between intent and purchase. Once the customer has set their preferences, budget, delivery details, and approval rules, the agent can complete the purchase when those conditions are met. That means fewer checkout steps, fewer delays, and fewer chances for the customer to drop off.

- Automate repeat purchases without locking customers into subscriptions: Agent-led commerce could make repeat purchases easier while giving customers more control than a standard subscription.

Instead of buying the same item on a fixed schedule, the agent could act only when specific conditions are met: for example, when the customer is running low, when the price is right, when a preferred product is available, or when a suitable substitute offers better value.

That makes repeat purchasing more flexible: the customer sets the rules, but the agent handles the timing, comparison, and checkout.

This is a high-level overview of where the opportunity sits. The reality for each merchant will depend on category, customer base, order value, and how much control they're willing to delegate.

The impact of agent-led commerce on payment control

Agent-led commerce doesn’t automatically move the customer journey outside the merchant’s control. The key question is where the agent sits.

If the agent sits inside the merchant’s own ecosystem, such as a shopping assistant like Amazon Rufus, the merchant keeps more control over the experience. It can decide how products are presented, what data is collected, which payment methods are offered, how transactions are routed, and how post-purchase support is handled. In that model, the agent becomes another layer of the merchant’s customer experience.

The risk profile changes when the agent sits inside a third-party interface, such as an LLM-based shopping assistant that helps customers compare products, build baskets, or initiate purchases without starting on the merchant’s site.

In that model, merchants may gain access to new customers or higher-intent purchase moments. But they may also lose visibility into the journey that led to the transaction. They may not know exactly what the customer asked for, what the agent recommended, which alternatives were shown, how the product was positioned, or why a particular payment method was selected.

That is where agent-led commerce becomes a payment control issue. When more of the journey happens outside the merchant’s owned environment, payment and fraud teams may receive less session data, fewer behavioural signals, and less control over how the payment is initiated, authenticated, authorised, and routed.

We're already hearing concerns from merchants. Laurene Lecomte, Director of Payments, Fraud, and Risk at Back Market, described agentic commerce as "a big opportunity, but also a threat," warning that merchants could lose control and visibility into fraud, after-sales, and loyalty if they are not prepared.

Read more from Laurene and other payment leaders in our merchant panel on AI in payments.

The payment-control questions merchants need answered

That creates a set of unanswered questions that every payment leader should be thinking about.

- Where did the customer come from? Without clear referral and journey data, it becomes harder to understand which channels are driving demand and how agent-originated traffic performs.

- What did the agent recommend? If the product, price, policy, or payment method was selected by an agent, merchants need to know what the customer was shown before they bought.

- What fraud signals are still available? Agent-led journeys may remove the browsing, device, session, and behavioral signals fraud tools rely on to separate good transactions from bad ones.

- Who captured consent and authentication? If the customer gave permission earlier in the journey, merchants need clarity on how that consent was recorded and who verified the customer was authorized to buy.

- Can you still control routing and payment choice? Payment teams need to know whether they can still choose the right PSP, payment method, fraud provider, or authentication flow.

- Who carries the risk if something goes wrong? The economics only work if merchants understand who owns disputes, fraud, chargebacks, failed orders, and customer support issues.

The operating model is still unclear. Liability, authentication, routing control, dispute handling, data sharing, regional requirements, and payment method support all need clearer frameworks before payment teams can assess the true cost and risk.

What works for a US card transaction may not translate cleanly to other regions, payment methods, or regulatory environments. A wallet-led flow, open banking payment, local payment method, or market with stronger authentication requirements may create a very different set of obligations.

And until the data, liability, economics, and routing implications are clearer, it’s hard to feel confident that the benefits outweigh the risks.

How agentic commerce reduces fraud visibility

Agentic commerce changes the fraud equation because it changes who is present in the flow.

In a traditional checkout, merchants and fraud providers can assess the customer across the journey: how they arrived, how they browsed, what they added to their basket, which device they used, whether the billing address matched, how they behaved at checkout, and how the payment was authenticated.

When an agent sits between the customer and the merchant, some of that context disappears. If the agent discovers the product, builds the basket, and initiates the transaction, the merchant may only see the final payment request, with no visibility into the behavior that should explain whether it should be trusted.

Jeff Otto, Chief Marketing Officer at Riskified, put it plainly: "You're losing somewhere around a third of the signal that most platforms use to make informed decisions: to make sure that the good customers get approved and the bad fraudsters get denied.”

Riskified's own testing shows this in practice.

The team ran side-by-side tests using synthetic identities, pushing a fraudulent order through an early agentic checkout flow with a newly created email address, an incorrect billing address, and a VPN. The transaction was approved. When they ran the same order through the merchant's traditional checkout, it was declined and the account was blocked.

Listen to the full podcast: Payments Unfiltered | How AI shoppers are forcing merchants to rethink fraud with Jeff Otto

The data gap that comes with agentic commerce creates several risks for merchants:

- Less context for fraud scoring: Fraud tools rely on signals like device data, session behavior, browsing history, checkout interactions, location, velocity, and customer history. Agent-led flows may pass fewer of those signals to the merchant.

- More uncertainty around intent: In agent-led commerce, the customer may have given permission earlier in the journey. By the time the merchant sees the payment, intent has been delegated rather than expressed directly.

- More conservative risk decisions: If issuers, PSPs, or fraud tools receive less context, they may become more cautious. That can mean more declines, more false positives, or more friction for legitimate customers.

- Unclear liability: If a transaction turns out to be fraudulent, merchants need to know who carries the risk: the merchant, the agent provider, the PSP, the issuer, the wallet, or the customer.

The core issue is simple: fraud systems work best when they have context. If agentic commerce removes parts of the journey from the merchant’s view, payment and fraud teams may be asked to make decisions with less data, while still carrying much of the risk.

“Agent-led commerce can strip away the early journey signals fraud teams rely on. The merchant may still see the payment, but not the behavior that explains whether it should be trusted.”

— Theo Spyrides, VP Product, Primer

That's why the protocol question matters as much as the payment question. It's not enough for an agentic commerce standard to complete a transaction. Merchants need to know what data is passed, who owns authentication, how disputes are handled, and what happens when an agent-initiated payment goes wrong.

What does agent-led commerce cost merchants?

Some agentic payment models may add new fees on top of existing processing costs, putting more pressure on margins. For merchants already managing tight margins, the economics need to be tested carefully.

For instance, OpenAI reportedly charges a 4% checkout fee on Shopify merchants selling through ChatGPT.

The exact fee structure will vary by protocol and by merchant agreement, but this is a useful reference point: it shows that agent-led commerce can introduce a meaningful new cost layer, not a marginal one, stacked on top of the fees merchants already pay to sell online.

That's why payment teams can't evaluate agent-led sales on conversion alone. A transaction that looks incremental at the top line can look very different once you factor in platform fees, payment processing costs, fraud exposure, support overhead, and the loss of routing control.

The protocol problem behind agentic commerce

For AI agents to buy things on behalf of consumers, there needs to be a standardized way for agents, merchants, wallets, PSPs, and payment networks to communicate. That means defining how an agent checks product data, verifies inventory, passes customer intent, initiates payment, handles authentication, and confirms the order.

That's what agentic commerce protocols are trying to solve. But fragmentation at this stage isn't a surprise. 3DS applications have taken years to converge and stabilize. Scheme rules still diverge by network, region, and card type. Every time a new capability has emerged in payments, multiple competing standards have arrived before one—or none—has won.

Agentic commerce is following the same pattern.

PSPs are also racing to announce their own agentic commerce solutions, and it's adding to the noise rather than cutting through it:

- Stripe co-developed OpenAI's ACP and has its own Agentic Commerce Suite, already used by merchants including Best Buy, Coach, and Kate Spade

- Adyen launched Adyen Agentic, built to support UCP, ACP, and AP2 all at once

- PayPal has partnered with Mastercard to bring Agent Pay into its wallet, and is a named payment option inside Google's UCP rollout

Each protocol takes a different view of how agent-led transactions should work, and each reflects the incentives of the platform behind it. OpenAI's ACP has been discussed primarily in the context of one-off card-initiated transactions, with constraints around inventory refresh, orchestration, and PSP selection. That may work for simple purchases, but it doesn't map to how most enterprise merchants manage checkout today.

Google's UCP is arguably the more complete framing as it positions agentic commerce as a new sales channel rather than just a payment flow, which is closer to how merchants actually think about the problem.

But coherent framing doesn't guarantee adoption. OpenAI, the card networks, wallets, PSPs, and commerce platforms all have different incentives, and none of them are naturally inclined to converge on someone else's standard.

There is no doubt that these will evolve and become more complete in what they support, but the reality is that right now these are nascent technologies that do not cover the full scope of online commerce.

The challenge of choosing a protocol in 2026

‘Full’ agentic commerce coverage means potentially integrating with all four protocols, and each has a different architecture, data requirements, and commercial terms.

These aren't trivial builds. Each integration carries significant engineering costs, and none of them are guaranteed to become the standard.

If you commit resources to a protocol that doesn't gain adoption, gets superseded, or turns out to be incompatible with how you want to route payments or manage fraud, you've burned engineering time on infrastructure that doesn't serve your stack: and you'll have to do it again when the landscape settles.

What can merchants do now to prepare for agentic commerce?

Agentic commerce is too early and too fragmented for merchants to make a big protocol bet. But that doesn't mean payment leaders should wait. The window to prepare is now, before the changes arrive and decisions get made under pressure.

Don’t blindly buy into the hype

There's a lot of noise around agentic commerce right now, but not much proven utility yet. Merchants shouldn't feel pressure to rush in if it doesn't look right for their business.

Take the early results of ChatGPT's Instant Checkout with Shopify as an example of why you ought to avoid rushing in.

Out of the millions of merchants on Shopify, only around a dozen actually went live with the feature.

Shopify's own president said the bottleneck was on the AI firms' side rather than the merchants', since the protocol-based onboarding process hadn't scaled.

When shoppers did use it, conversion was weak: one analysis put Instant Checkout's conversion rate at 1.18%, with a cart abandonment rate of 77.45%.

OpenAI ultimately pulled back from in-chat checkout entirely, shifting its focus to product discovery instead, and Walmart replaced its own Instant Checkout integration with its Sparky chatbot after disappointing sales.

None of that means agentic commerce won't matter. It means the first widely-touted version of it didn't deliver the volume or reliability that the hype promised. Merchants should let the data, not the press releases, decide how much investment this deserves right now.

Make your products agent-readable

Agents need to understand what you sell before they can recommend it. That means product data needs to be structured, accurate, and easy for machines to interpret. Product descriptions, attributes, prices, availability, delivery options, and policies should be clear and accessible, not hidden behind messy metadata or complex rendering.

This is often described as Agent Engine Optimization, or AEO. It sits before the payment journey, but it matters because discovery will shape which merchants agents surface in the first place.

Monitor LLM referral traffic

Merchants should start tracking how much traffic is already coming from AI tools and LLM-based discovery. Today, that traffic may be small, but it gives you an early signal of how customer behaviour is changing.

Look at referral sources, landing pages, conversion rates, basket composition, and payment method mix. If agent-originated sessions behave differently from search, social, affiliate, or direct traffic, payment teams need to understand why.

Map the data and fraud signals you could lose

If more of the journey happens outside your owned checkout, you may lose access to the behavioural signals you currently use to assess risk and optimise conversion.

Payment leaders should map which signals they rely on today: device data, session behaviour, basket changes, customer history, velocity checks, location data, authentication signals, and fraud provider inputs. Then ask what happens if an agent controls discovery, basket creation, or payment initiation before the customer reaches your checkout.

Don’t pick a protocol winner yet: preserve your flexibility

The protocol landscape is still unsettled. OpenAI, Google, Visa, Mastercard, Stripe, PayPal and others are moving in different directions, and it’s not yet clear which models will gain merchant or consumer adoption.

That makes flexibility the priority. Merchants should avoid hard-coding themselves into one agentic commerce model before commercial models, liability frameworks and technical standards are clearer.

Instead, focus on keeping your payment infrastructure adaptable. You need the ability to connect new providers, test different payment methods, route transactions intelligently and change your setup as standards develop.

Agentic commerce may become a valuable sales channel, but merchants should not give up control of payments, fraud, data or customer experience without knowing what they are getting in return.

Why Primer is watching closely but not rushing in

Primer has been actively engaged in the protocol discussions shaping agentic commerce, and we have a dedicated task force tracking how the space develops.

But right now, we're not seeing real merchant appetite to invest in agent-led payments at any meaningful scale. So rather than making noise about protocols that aren't ready, our focus is on solving problems that are.

New technology is exciting, and there's no doubt agentic commerce will change how commerce happens online. But new technology is a means to an end, not an end in itself, and the merchant perspective hasn't been represented nearly enough in the solutions presented so far.

We take our duty to advocate for merchants seriously, and that means being honest about where things stand. The fragmented protocols on offer today are early, short on evidence of real utility, and have in some cases created more problems for merchants than they've solved. We're actively working on how best to address that, but we won't contribute to the hype cycle just to be seen moving. Instead, we'll keep working closely with merchants, on Primer and beyond, on how to get the most out of this technology when it's actually ready to deliver for them.

Engage with agentic commerce on your own terms

Agentic commerce is coming, but merchants don’t need to hand over the keys before the model is proven.

Prepare for the discovery shift. Make your products readable, track AI-originated traffic, and understand what data you could lose if checkout moves elsewhere.

But don’t rush into a protocol bet. Stay flexible and stay close to the market.

Make sure any move into agent-led payments protects the control you’ve spent years building.

Primer is building a unified intelligence for payments, giving finance and payment teams a full picture of every transaction, and the tools they need to act. If you’re new to Primer, book a demo with our team to see how we can help you stay flexible and optimize your payment strategy.

Frequently Asked Questions (FAQ): Agentic commerce

What is the difference between agentic commerce and AI-powered checkout optimization?

Agentic commerce involves AI agents acting as intermediaries across the shopping journey, from product discovery and product recommendations to purchasing decisions and, in some cases, payment initiation. AI-powered checkout optimization uses machine learning to improve existing human-led payment workflows, such as smart routing, dynamic 3DS, or fraud decisioning, to increase approval rates.

Do merchants need to do anything about agentic commerce right now?

Yes, but the focus should be on discovery rather than payments. Consumers are already using conversational interfaces and shopping assistants like ChatGPT, Gemini, Claude, and Amazon’s Rufus to research products and make purchasing decisions. Merchants should make sure their product catalogs are machine-readable so AI agents can accurately discover, compare, and recommend their products.

What is Agent Engine Optimization and how is it different from SEO?

SEO is about helping human shoppers find your site through traditional search engines. Agent Engine Optimization, or AEO, is about helping shopping agents and large language models understand your product data, policies, inventory, prices, and delivery options. The goal is to make your store easier for AI-driven discovery systems to read, index, and reason about.

What are the main use cases for agentic commerce?

The most realistic near-term use cases are discovery-led. For example, a customer might ask a personal shopper-style AI assistant to compare running shoes, find a hotel with free cancellation, or recommend a skincare product for a specific budget. More advanced use cases involve repeat purchases, replenishment, subscriptions, or other rules-based workflows where an agent could help streamline the buying process.

How does agentic commerce affect payment fraud?

It complicates payment fraud because agents may bypass the early-journey session data that fraud tools use to assess risk. If product discovery, comparison, and checkout happen inside an agent-controlled interface, merchants may receive less context about the customer’s behavior. That can lead to less accurate fraud scoring, more conservative risk decisions, and potentially higher liability for the merchant.

What happens after the purchase in agentic commerce?

Post-purchase workflows are still an open question. Merchants need to understand who handles refunds, cancellations, customer support, delivery updates, disputes, and returns when an order is initiated by an agent. The payment is only one part of the lifecycle. Agentic commerce also needs clear rules for everything that happens before and after the transaction.

.avif)

.avif)