For merchants, payments can feel like a black box. Money flows in, money flows out, but along the way, revenue quietly slips through the cracks.

Sometimes, valid transactions are declined and never retried. Fraud controls end up blocking fraud…but also good customers. Other times, clunky checkout flows drive cart abandonment.

Each of these issues on its own looks minor. But at scale, across thousands or even millions of transactions, they add up to a serious drain on growth and impact your bottom line.

This guide breaks down the four areas where merchants most often lose money and shows how to turn them into opportunities for optimization and growth.

Stop letting failed payments, high fees, and checkout friction eat into your margins. Book a demo with our team today.

What is revenue optimization in payments, and why does it matter?

Revenue optimization in payments is about making sure every sale that should go through does.

For merchants, optimizing payments means capturing more revenue without acquiring new customers, turning the checkout into a growth driver rather than a cost center. It means higher authorization rates, lower fees, smoother customer journeys, and faster access to funds.

In short, it’s about unlocking revenue that is already within reach and using payments as a competitive advantage.

Four key areas merchants can optimize to take home more revenue

Across the payment lifecycle, four areas consistently emerge as the biggest sources of revenue leakage:

- Authorization rates: Too many valid transactions fail at the final step, costing sales and damaging customer trust.

- Payment costs: High interchange, processing, and network fees quietly eat into margins.

- Fraud controls: Rules that are too strict block genuine customers, while loose ones drive up chargebacks and fraud losses.

- Checkout experience: Clunky or confusing checkout flows cause unnecessary abandonment, even from customers ready to pay.

Optimizing for payment authorization

Payment authorization represents the moment of truth in every transaction. When a customer's payment fails to authorize, the sale is immediately lost, along with potential future revenue from that customer relationship.

Here are five proven strategies to help you recover more transactions and boost approval rates:

1. Use smart retries

Many declines are temporary. Intelligent retries let you recover payments affected by issuer downtime, network issues, or PSP outages. Routing a retry through another processor can instantly save the transaction.

2. Use intelligent authentication

Modern authentication tools assess risk in real time so only higher-risk transactions require extra verification. This keeps checkout friction low for trusted customers while giving issuers the signals they need to approve more payments.

3. Reduce false declines

Fraud tools should stop bad actors, not good customers. Review and tune risk rules, use machine-learning signals, and regularly check edge cases to avoid unnecessarily blocking legitimate transactions.

4. Improve checkout data quality

Providing clean, accurate billing and device data helps issuers validate transactions more confidently. Keep the checkout flow simple, but include the essential details that increase approval accuracy.

5. Route transactions to the best-performing processor

Processor performance varies by region, issuer, card type, and time of day. Route transactions based on historical success patterns to significantly increase authorization rates.

Read more here: Five ways to improve your payment authorization rates

2. Cost management and fee reduction: cutting through hidden costs

Payment processing fees topped $187 billion in the U.S. in 2024, according to the latest Nilson Report. For merchants, those costs eat directly into profit margins, yet many still lack clear visibility into where fees are piling up or how to reduce them.

From interchange and network fees to processor markups and chargebacks, the layers of cost quickly add up. Without a strategy to manage them, merchants leave money on the table every day, with every transaction.

Strategic cost management requires both tactical and structural changes:

- Develop a multi-acquirer strategy: Multiple processors competing for your business enables better rate negotiations and optimal routing

- Use cost-effective payment rails: Domestic schemes like Cartes Bancaires in France are significantly cheaper than international networks

- Encourage lower-cost payment methods: Account-to-account payments like ACH, SEPA Instant, and PIX eliminate intermediaries and reduce costs

- Optimize interchange qualifications: Include ZIP codes and Level II/III data to qualify for lower rates in unregulated markets. Use the correct Merchant Category Code to ensure you're classified in the appropriate risk category to secure optimal rates

- Implement network tokens: Visa and Mastercard offer preferential pricing for tokenized payments since 2023

Read more: How to reduce card payment fees

3. Fraud prevention: balance protection with customer experience

Global online payment fraud losses were estimated at nearly US$35 billion in 2024. Yet overly aggressive fraud prevention can be equally costly, blocking legitimate customers and damaging long-term relationships.

The challenge lies in finding the optimal balance: robust enough to prevent fraud and flexible enough to avoid false positives that drive away genuine customers.

Effective fraud detection and prevention requires layered security measures without customer friction:

- Implement multi-factor authentication: Use biometrics, device fingerprinting, and behavioral analysis.

- Deploy Address Verification Service (AVS): Cross-reference billing addresses with issuer records.

- Require CVV verification: Confirm physical card possession.

- Use 3D Secure strategically: Trigger authentication only when risk indicators justify it.

- Leverage specialist fraud tools: Work with providers like Riskified, Forter, or Signifyd for advanced detection.

- Use network tokens: Reduce fraud and improve approval rates by replacing raw card numbers with secure tokens.

- Block suspicious BINs: Add friction or declines for BIN ranges consistently associated with fraud or high chargebacks.

Read more: How to prevent online payment fraud: the complete guide

4. Optimizing the checkout experience by removing friction

Nearly 70% of customers abandon shopping carts before completing their purchase, according to a report by Baymard.

Strategic checkout improvements focus on reducing friction while building trust:

- Offer guest checkout: Enable purchases without mandatory account creation

- Display costs upfront: Show shipping, taxes, and fees early in the process

- Embed checkout on-site: Avoid redirecting customers to external payment pages

- Optimize for mobile: Ensure seamless experiences across all devices

- Include trust signals: Display security badges, customer reviews, and return policies prominently

- Provide preferred payment methods: Research regional preferences and local payment options

- Auto-fill information: Use address lookup and saved payment methods to reduce form completion time

Read more: How to optimize your checkout

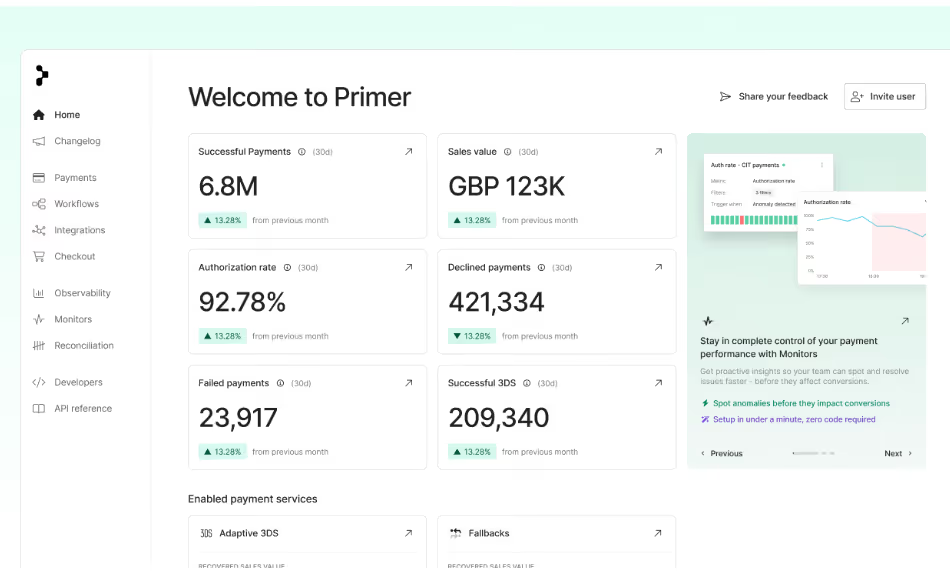

How Primer can help you optimize your payment revenue

Most merchants recognize they are losing money in payments, but fixing the issue often requires juggling multiple providers, clunky tools, and endless engineering requests. The result is a fragmented stack that still doesn’t give you full control.

Primer takes a different approach. Our unified payments infrastructure brings every method, processor, and optimization tool into a single platform. Instead of stitching together point solutions, you orchestrate your entire payment strategy through Primer’s no-code interface: testing, optimizing, and scaling without bottlenecks.

Here’s how you can use Primer to optimize your payments:

Stop soft declines in their tracks with Fallbacks

Not every decline has to mean a lost sale. Many transactions fail due to recoverable reasons, such as processor downtime, temporary issuer rules, or regional quirks. Primer’s Fallbacks let you decide exactly how those transactions should be retried.

You set the criteria. For example, route high-value transactions to the acquirer with the strongest approval rates in that market. Or, if one processor is experiencing latency, send the retry through a backup instantly. The logic is yours to define: Primer makes it simple to configure without code.

Instead of leaving customers stuck at checkout with no way forward, the retry happens invisibly in the background. The customer completes their purchase without interruption, and you capture revenue that would otherwise have been written off.

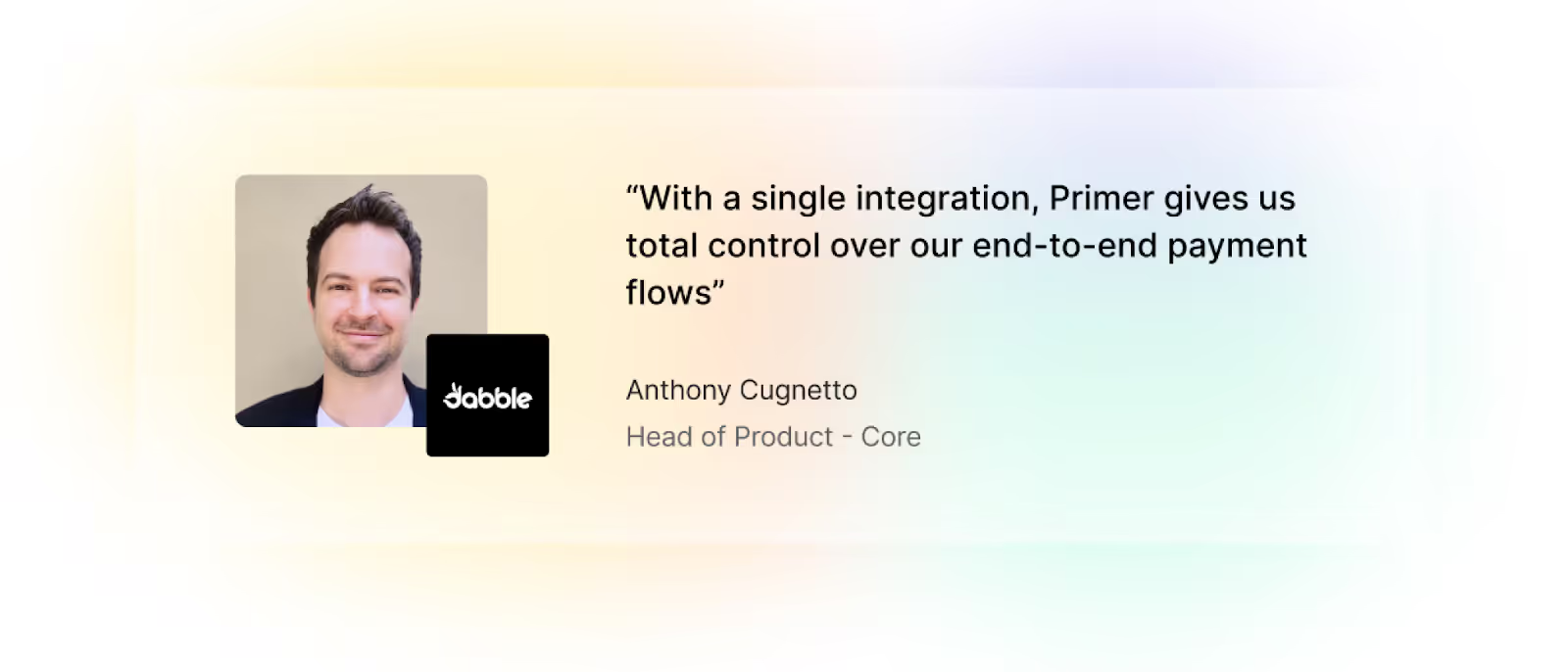

That’s how Dabble, a fast-growing betting app, used Primer to reach a 96% authorization rate during the 2023 Melbourne Cup and recover nearly $50,000 in sales that would otherwise have been lost.

Read the full case study: Dabble picks a winner by partnering with Primer

Cut costs by adding PSPs in clicks and tracking performance

Processing fees aren’t set in stone, but many merchants pay more than they should because adding or switching PSPs feels like a huge integration project. Primer removes that barrier.

With just a few clicks, you can connect new processors directly through our platform. The more providers you have in play, the stronger your hand when it comes to negotiating rates and routing transactions through the most cost-effective option.

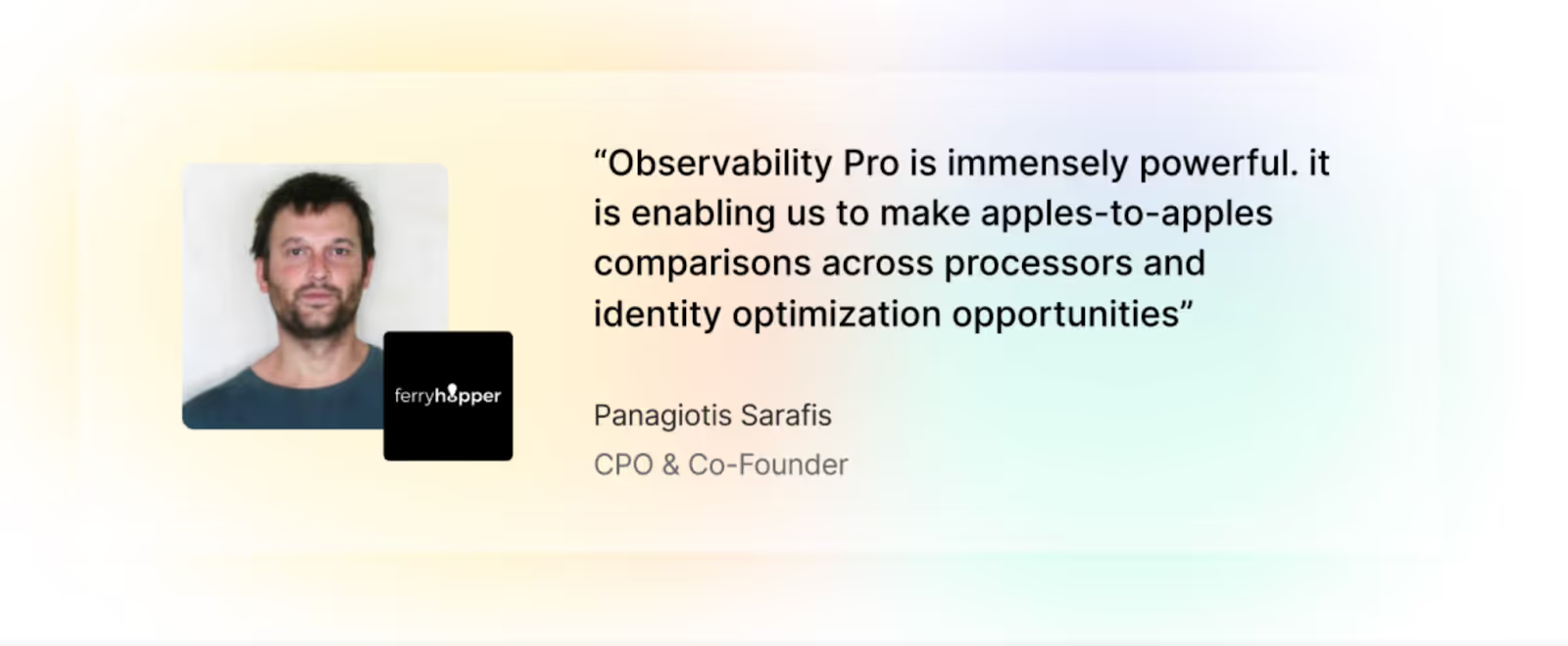

And with Primer’s Observability dashboard, you get a unified view of how each PSP is performing in real time, from authorization rates to cost efficiency, so you can base your payment routing and negotiations on hard data, not assumptions.

That’s exactly how Ferryhopper, the global online ferry booking platform, has scaled its payments. Operating across 12 countries with five PSPs, Ferryhopper uses Workflows to optimize routing for cost and performance, while Observability gives them the data to experiment, compare processors, and uncover new optimization opportunities.

Read the full case study: Charting a new course for payments at Ferryhopper

Balance fraud protection and conversion

Primer integrates with leading fraud vendors like Riskified, Forter, and Signifyd through a single connection. That means you can:

- Layer multiple providers for extra protection

- Switch or test tools without heavy engineering

- Fine-tune rules to reduce false declines

For customers, it all happens invisibly. Genuine transactions glide through with minimal friction, while suspicious ones face stronger checks. The result: fewer chargebacks, fewer false declines, and more revenue captured.

And this is just one use case. Workflows aren’t limited to fraud management: the same drag-and-drop logic can optimize routing, fees, authentication, and checkout flows.

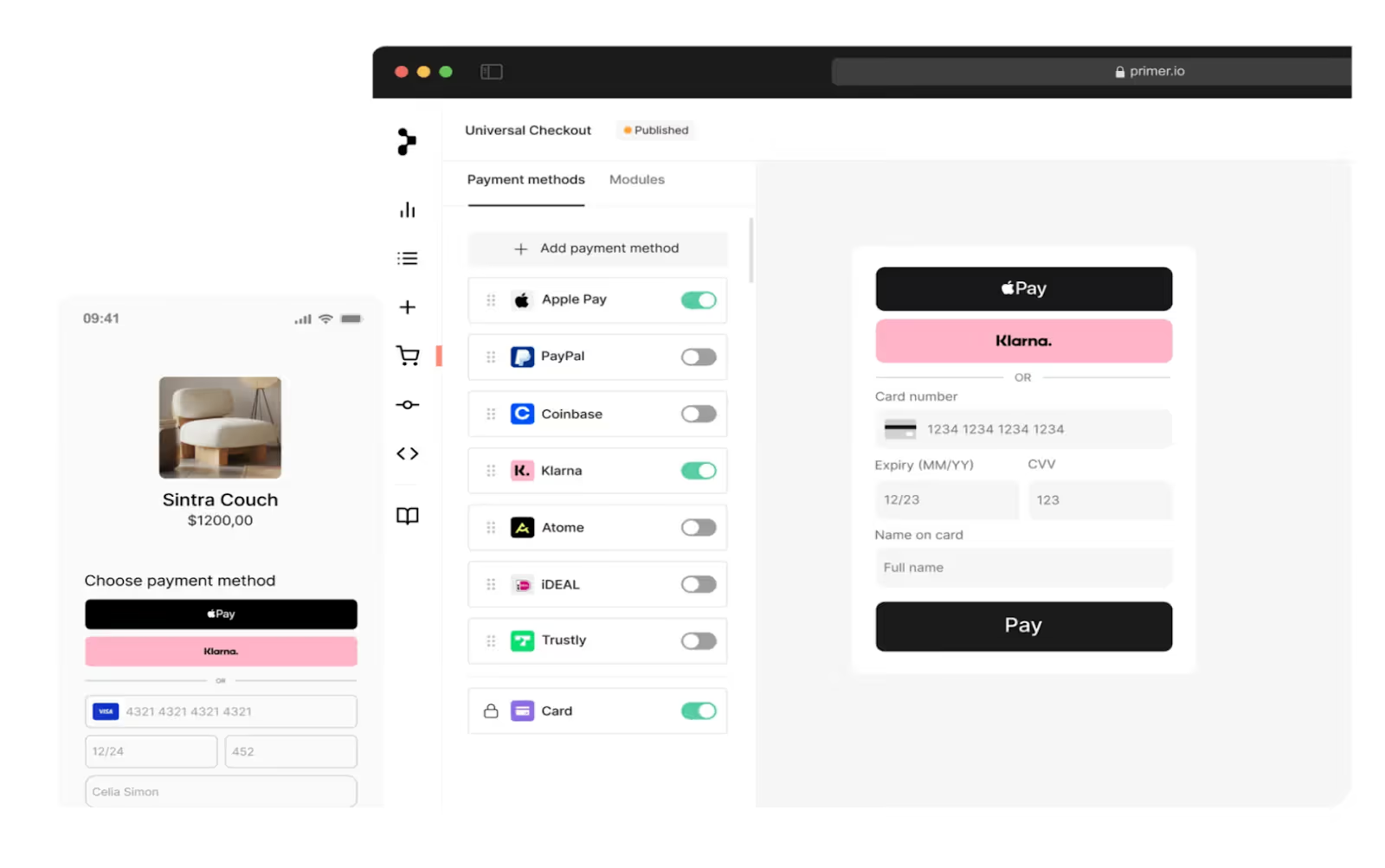

Reduce the friction with Primer Checkout

Adding new alternative payment methods should be simple. With Primer’s unified infrastructure, you only need to integrate once. From there, you can activate the methods your customers expect in just a few clicks. That includes digital wallets like Apple Pay and Google Pay, BNPL services like Klarna or Afterpay, and local options like iDEAL or PayNow.

Once you go live, Primer Checkout gives you complete creative and technical control over your payment experience without adding engineering overhead.

You can:

- Dynamically tailor payment methods by market, currency, device, and basket logic to surface the most relevant options

- Fully customize every element to match your brand with no templates or workarounds

- Continuously experiment with layouts, flows, and routing rules to maximize conversion and reduce drop-off

Primer lets you design, launch, and optimize a checkout experience that adapts to every customer in real time and scales with your imagination.

This makes checkout easy to adapt, experiment with, and refine until it delivers the smoothest possible payment experience for your customers.

That is exactly what Conforama, one of Europe’s largest home furnishings retailers, achieved. By using Primer, they rolled out new local payment options faster, improved authorization rates, and created a checkout that truly reflects their brand.

Read the full case study: Reimagining the role of payments at Conforama

From hidden leaks to a payment growth engine with Primer

Revenue optimization is about turning payments into a lever for business growth. With Primer, you’re not limited by legacy systems, manual processes, or engineering bottlenecks. You have one platform to raise authorization rates, cut unnecessary costs, balance fraud with conversion, and deliver a checkout experience that wins customers over.

This results in more revenue captured, less waste, and a payment strategy you fully control.

Book a demo to get started today.

FAQ: Revenue optimization in payments

1. What is payment revenue optimization?

Payment revenue optimization is the process of maximizing revenue capture while minimizing costs and friction across the payment lifecycle. It focuses on authorization rates, fees, fraud, and checkout performance.

2. How can merchants improve payment authorization rates?

You can increase authorization rates by using smart routing, fallbacks, network tokenization, and tools like Primer 3DS. These approaches ensure more legitimate transactions succeed.

3. How do I reduce payment processing fees?

Merchants can cut costs by routing through cheaper acquirers, enabling lower-cost methods like Open Banking or ACH, and monitoring fee data with reconciliation tools to identify hidden charges.

4. What’s the best way to balance fraud prevention with conversion?

The best approach is layered. Use multiple fraud providers, apply 3DS only when it improves approval rates, and adapt rules as risk profiles change. This avoids blocking genuine customers while reducing fraud.

5. Why does checkout optimization impact revenue?

A well-designed checkout reduces cart abandonment. Offering the right payment methods, currencies, and a smooth on-brand flow can significantly increase completed transactions and customer satisfaction and trust.

.png)

.avif)