French shoppers expect choice. At checkout, they want to see the global and local payment methods they already trust: cards, wallets, or bank transfers. For merchants expanding into France, the challenge isn’t knowing which methods matter. It’s supporting them all without draining resources, and proving that they actually lift conversions.

In this guide, we’ll walk through the essential payment methods you need to succeed in France, then show you how to build a payment stack that makes it simple to add them without slowing your team down.

Book a call with Primer now to learn how you can build out your French payment stack without the engineering lift.

Which payment methods should you offer in France?

1. Credit and debit cards

In France, card payments account for 48% of all transactions. Between the two, debit cards are significantly more common. What makes France interesting is how you handle card payments.

Over 65% of all French card transactions are processed by the domestic card scheme Cartes Bancaires.

Most Cartes Bancaires cards are also co-branded with Visa or Mastercard, so certain payments, like international payments, can be routed through these major networks.

For merchants, routing payments made in France through Cartes Bancaires can mean:

- Significantly lower interchange and processing fees

- Higher authorization rates and less 3DS friction due to better connections with local infrastructures

Displaying the familiar “CB” logo at checkout can also act as a “trust seal” for French customers, with the potential to boost conversions and confidence in your brand.

Looking for a payment solution to help you integrate with PSPs that support Cartes Bancaires? Book a demo to see how Primer can help

2. Digital wallets and account-to-account payments (A2A)

Digital wallet payments account for around a third of all online purchases in France, with PayPal currently dominating market share.

PayPal alone accounted for about 18% of all online payments in France in 2024, and France ranks among the top five countries worldwide for PayPal usage, along with the US, Germany, the UK, and Italy. PayPal also offers French customers a Buy Now, Pay Later option to pay in four installments.

However, there are other digital wallets, as well as A2A payments, to consider offering:

Google, Apple, and Samsung Wallets

According to one 2024 PYMNTS study, 18.6% of French customers had used Apple Wallet in the past year, while 8.7% of customers had used Google Wallet, and 4.4% had used Samsung Wallet. About two-thirds of all French digital wallet users point to Apple Wallet as their preferred digital wallet for online shopping.

Lydia/Sumeria

Originally launched as a peer-to-peer (P2P) payments platform, the Lydia super-app now has over 8 million users, and has expanded to include digital wallet capabilities and a Shopify integration. In 2024, it announced that it was splitting into two apps, Lydia for P2P payments and Sumeria for banking functions.

Today, a Lydia shopper clicks ‘Pay with Lydia’ on a merchant’s website. They then receive a notification, confirm in-app, and authenticate with biometrics. Behind the scenes, funds a card or bank account.

Fintecture (Open Banking A2A)

Fintecture is a French-based open banking payments provider that enables merchants to accept bank transfers as first-class payments. Their “Immediate Transfer” product allows for seamless account-to-account payments, with full reconciliation, real-time status, and fraud protection built in.

Because Fintecture operates under French regulation (Banque de France / ACPR) and natively connects to French banks, it can offer strong local acceptance, lower friction, and deeper integration with the French banking ecosystem.

Paylib and Wero

Popular local digital wallet Paylib has at least 35 million registered users in France, and is connected with CB and a consortium of major French banks, including Banque Postale, BNP Paribas, Société Générale, and Crédit Agricole. Paylib works similarly to other digital wallets, but take note: in order to start using Paylib, customers must link a credit or debit card to their Paylib accounts.

This detail is significant because, for the past several years, Paylib has been slated for discontinuation and replacement by the account-to-account (A2A) app Wero. Developed by the European Payments Initiative (EPI), Wero is built on top of the SEPA instant transfer system, which pulls funds directly from the customer’s bank account. Wero does not require a credit or debit card.

Update: Wero has now launched in France for instant account-to-account payments between individuals, taking over from Paylib as France’s local wallet landscape shifts toward a pan-European alternative. The next major step is merchant acceptance: EPI says Wero’s ecommerce payment solution is rolling out in 2026, with France and Belgium following Germany. For merchants, that makes Wero worth tracking now, even if its ecommerce acceptance is still developing.

Learn more: Wero payment method explained: the new European wallet replacing iDEAL and Payconiq

3. Buy Now, Pay Later (BNPL)

The French BNPL market size is valued at about 20 billion USD as of 2025 and expected to reach 42 billion USD by 2023, with 69.8% of that share coming from online sales. Per one study, 70% of French citizens have used BNPL at some point, and 44% have used it repeatedly.

Per that same study, more than half (52%) of the French population plans to either maintain or increase their BNPL use in the future. Meanwhile, travel & leisure is the fastest-growing category for BNPL in France, with a 19.1% CAGR. 68% of French fashion chains now offer at least one BNPL solution.

For merchants scaling into France, BNPL is now an essential payment offering.

Klarna

Klarna is among France’s top BNPL providers, with over 825,000 active app users. French customers can choose to pay immediately, pay in three installments, or delay payment until 30 days after making their purchase, with no fees or interest. Klarna also offers repayment plans with terms of up to 24 months (36 in some markets).

PayPal Credit

In France, PayPal customers can choose to make their payments in four interest-free installments, with zero interest or fees. The option is available for purchases of €30 to €2,000.

Alma

As of July 2025, Alma is the most popular local BNPL option in France, and the most popular BNPL method overall after Klarna and PayPal. The service lets merchants offer a handful of different payment arrangements: they can pay in 2, 3, or 4 installments for most purchases.

Alma users can also select a “Pay later” option that doesn’t involve any installments, but lets them defer payment by 15 or 30 days, and then pay for their purchase in full on a set date.

Alma is also introducing an option to finance larger purchases in up to 12 payments, but merchants who want to offer this service must join a waiting list, which will prioritize access for current Alma clients.

Other local BNPL methods in France

While Alma is the most important local method to offer, merchants could also consider additional providers:

- Oney

- Floa

- Scalapay

- Mondu

Read more: Alternative payment methods: offer customers more ways to pay

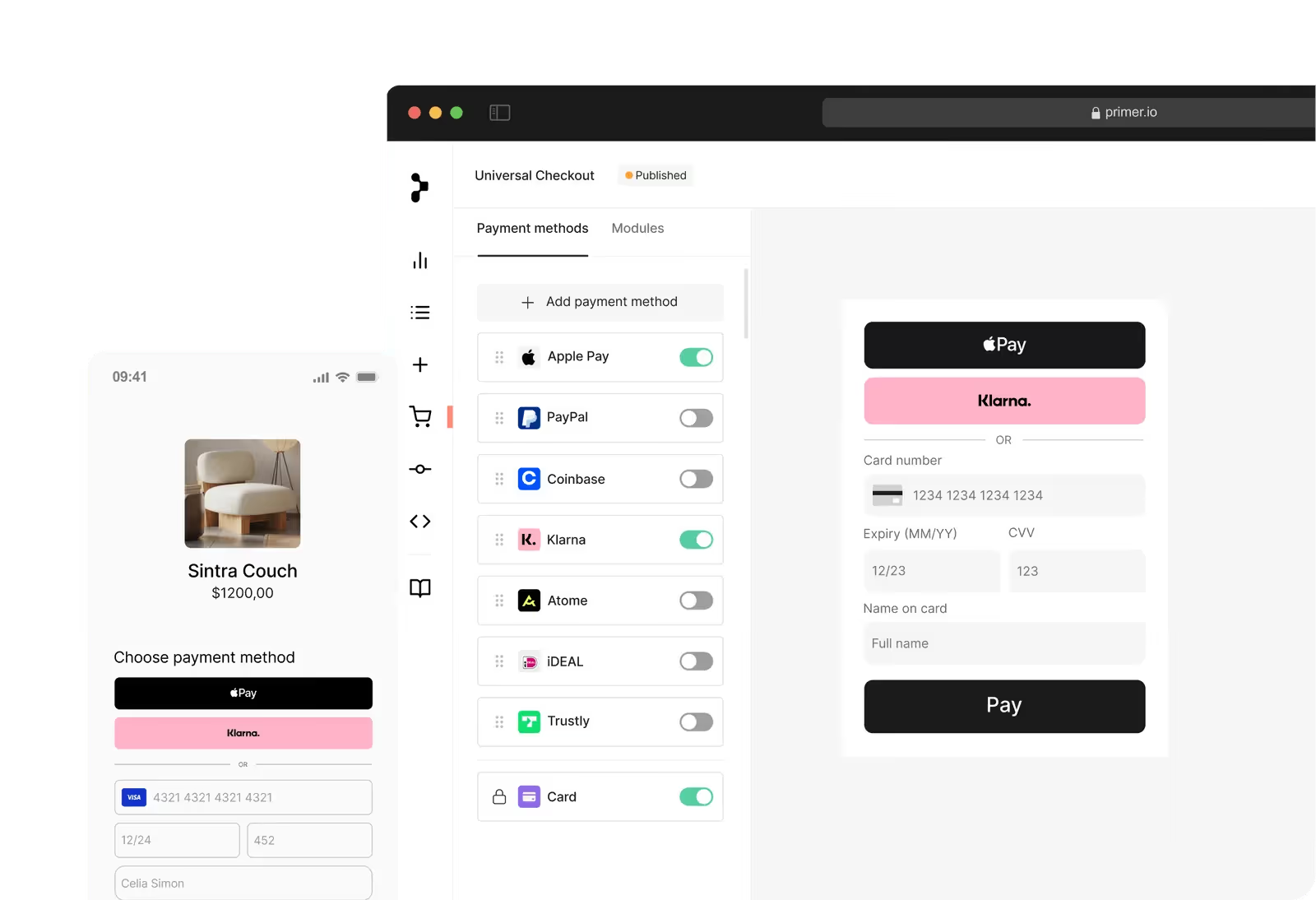

How Primer simplifies scaling into France

Adding new payment methods sounds simple. In practice, it means new APIs, weeks of dev work, and endless maintenance.

In France, the challenge is even sharper. Customers expect a mix of cards, wallets, and bank transfers, and the landscape is always shifting. Legacy systems and new tech overlap, making the logic more complicated every year.

As your business grows, the complexity only multiplies. Instead of driving innovation, your team ends up firefighting.

That’s why we built Primer. We take care of the messy details, so your team can get back to building.

With the world’s first unified payment infrastructure, every payment provider, tool, and service connects through a single platform.

With Primer, you can:

- Add new payment processors, like Adyen or Mollie, with just a few clicks, and instantly unlock local card schemes like Cartes Bancaires (which is crucial in France)

- Activate new global and payment methods like PayPal, Apple Pay, Klarna, Alma in minutes, without any code

You can also use our checkout builder to determine which payment methods your customers see based on factors like region, device, and cart value.

Use Workflows to implement smart payment routing without any code

Once you’ve activated the payment methods you want, use Workflows to create a flexible pathway for each payment. Simple drag-and-drop features let you easily build complex, customizable routing logic, based on factors like:

- Geography

- Transaction amount

- BIN (Bank Identification Number)

- Card type

For example, if you want to save costs or boost performance on card transactions, you can default to using Cartes Bancaires rails for French BINs when paying within France.

Finally, Primer Observability enables easier A/B testing by unifying payment data across all your processors. With just one dashboard, you can:

- Compare performance or conversions across BNPL methods like Alma vs Klarna

- See how much money you’re saving with Cartes Bancaires

- Understand how much revenue you’re recovering with Fallbacks

- Learn what’s causing payment declines, like certain BINs or 3DS settings

Read more: The art and science of A/B testing in payments

Case study: How Maisons du Monde scaled French payment methods with Primer

Maisons du Monde, the French home décor brand selling online and in-store across 11 European countries, faced mounting complexity as it tried to meet local payment preferences. Customers abandoned carts if their preferred methods weren’t available, but each new integration took months to build and maintain.

With Primer, Maisons du Monde quickly added essential methods like iDEAL and Bancontact, and used Primer’s checkout tool to control which options appeared based on each basket. Workflows let them route payments intelligently, ensuring higher success rates while cutting operational overhead.

By consolidating everything through Primer, Maisons du Monde turned payments from a blocker into a growth driver: offering the right mix of local methods to boost conversions without draining engineering resources.

Read the full case study: Maisons du Monde redesigns its payments with Primer

Integration complexity simplified, in France and beyond

When you’re staking out new territory, the last place you should be is down in the trenches, with your head buried in the code. Your focus belongs on strategy: understanding new audiences, testing bold ideas, and delivering better experiences at scale.

Primer makes it possible by pre-solving the unique technical challenges of each new region and market, so you don’t have to. We handle the hyper-local, so you can stay focused on your global vision for growth.

Book a demo to see how easy it is.

Frequently asked questions (FAQs)

Why is Cartes Bancaires essential for online payments in France?

Cartes Bancaires (CB) is France’s domestic card scheme and processes the majority of card transactions in the country. While CB cards are co-branded with Visa or Mastercard, routing payments through the local CB network typically results in lower interchange fees, higher authorization rates, and less friction with 3DS. Supporting CB directly is therefore critical for cost savings and performance when selling to French customers.

Do I need to support both Visa/Mastercard and Cartes Bancaires in France?

Yes, supporting both global and local card schemes is recommended. Although most French cards carry Visa or Mastercard branding, transactions processed through Cartes Bancaires often perform better domestically. With Primer’s Unified Payment Infrastructure, you can route French BINs through CB for local optimization, while using Visa or Mastercard as a fallback to recover revenue from failed payments.

What are the most popular payment methods in France right now?

French consumers use a mix of traditional and alternative payment methods, including credit and debit cards (mainly routed via the Cartes Bancaires network), digital wallets like PayPal, Lydia/Sumeria, Wero, and Apple Pay, BNPL (Buy Now, Pay Later) solutions like Alma and Floa, and SEPA Direct Debit.

How is BNPL adoption in France different from other markets?

France has seen explosive BNPL growth, with 20B USD market value in 2025, expected to more than double in the coming years. Notably, 69.8% of BNPL volume comes from online purchases, and over half of French BNPL users plan to maintain or increase usage. This makes BNPL an essential part of the French payment mix, particularly in the fashion and travel sectors.

Why is integrating French payment methods so complex?

France’s payment ecosystem is fragmented, with many local banks using legacy infrastructure and requiring custom routing logic. Integrating Cartes Bancaires, SEPA, local digital wallets, and BNPL providers in-house is time-consuming and resource-heavy. Primer simplifies integration by letting merchants add new payment methods with just clicks, optimize routing with drag-and-drop Workflows, and easily monitor performance from a single control center.

.png)

.avif)