Your customer is ready to buy. The products are in their cart, the price is right, and delivery looks good.

Then they hit the checkout, and their preferred payment method isn’t there. Maybe they were expecting Apple Pay or a BNPL option. They hesitate, drop off, and the sale disappears.

This is one of the most common and costly issues in ecommerce. According to Primer research, nearly 7 in 10 shoppers abandon their cart when they can’t pay the way they want.

There are two main challenges here:

- Knowing which payment methods to offer. Add too few and you’ll lose customers who can’t pay the way they want. Add too many and you risk higher costs and unnecessary complexity.

- Managing the technical side of payments. Each new method has its own integration requirements, and even something as simple as adjusting your checkout flow can take valuable engineering time. For growing merchants, that technical overhead can quickly slow expansion and drain resources.

In this guide, we’ll help you navigate both challenges. We’ll start by running through five of the most common payment method types in ecommerce and the benefits of offering each. Then, we’ll show how Primer can help you add and manage them without the technical burden.

Primer is a unified payment infrastructure platform that enables you to add new payment methods in just a few clicks. Book a no-obligations call with our team to discuss how we can help your business grow.

The six best payment methods for ecommerce: an overview

1. Debit and credit cards

It goes without saying that debit and credit cards are the most widely used and trusted payment methods in ecommerce. Virtually every online store offers this option at checkout.

Both payment types are processed through traditional card networks, which involve multiple intermediaries:

- The merchant’s payment gateway sends the transaction to the acquiring bank (the merchant’s bank).

- The acquirer forwards it to the card network (such as Visa, Mastercard, or American Express).

- The card network then routes the transaction to the issuing bank (the customer’s bank) for authorization.

Card payments are essential for merchants: they’re expected, widely supported, and trusted. But as ecommerce continues to evolve at a rapid pace, new alternative payment methods are emerging that promise faster, cheaper, and more seamless ways to pay. Keep reading to learn more about them.

A note on domestic card schemes

Domestic card schemes are payment networks that operate within a single country, issuing cards and processing transactions locally. Examples include RuPay in India, Dankort in Denmark, and Cartes Bancaires in France.

They’re still card payments: they just run on local rails instead of international networks like Visa or Mastercard. This typically means lower processing costs for merchants and higher trust among domestic shoppers.

In many cases, these cards are co-branded, using the domestic network for local transactions and switching to the international one when used abroad.

2. Account-to-account (A2A) payments

A2A payments move funds directly from the customer’s bank account to the merchant’s, bypassing card networks entirely and avoiding their associated fees.

With A2A payments, the customer authorizes the transfer through their bank, usually via a mobile app, using Strong Customer Authentication (SCA). This means they confirm their identity using at least two security factors, such as a password, a device, or biometrics (e.g., fingerprint or Face ID). Once approved, the funds are sent to the merchant instantly.

There are three main types of A2A payments:

- Bank transfers: Traditional manual transfers between accounts.

- Open banking payments (also known as Pay by Bank): API-powered transfers that connect merchants and banks directly. They’re fast, low-cost, and built on regulations like PSD2 in Europe.

- Local bank payment schemes: Country-specific systems that let customers pay directly from their bank account using trusted local rails.

Why should you offer A2A payments?

- They’re typically cheaper than credit and debit card payments, thanks to lower transaction fees and no card network fees

- Strong bank authentication requirements reduce fraud, and the risk of chargebacks is eliminated with this payment method

- Domestic A2A payments usually settle instantly, improving cash flow

- In markets with low card usage or among demographics that favor bank transfers, offering A2A payments can significantly reduce checkout drop-off and improve conversion rates

Popular A2A methods: Trustly, Volt, Sofort, and iDEAL.

3. Buy Now, Pay Later

Buy Now, Pay Later (BNPL) allows customers to make purchases online and pay in installments over time, often interest-free for a set period. Unlike with credit cards, merchants get paid upfront by the BNPL provider, while the customer repays the provider itself.

The BNPL provider is responsible for performing credit checks and risk assessments before approving the transaction. Since they manage all customer repayments, the merchant carries no direct credit risk.

Projections indicate that more than 670 million people worldwide will use BNPL by 2028.

Why should you offer BNPL?

- Research by Klarna claims that offering BNPL can increase the average order value by up to 68% and increase the conversion rate by up to 30%

- By not offering BNPL, you could lose as many as 43% of customers who regularly use this service.

- Learn more here: Buy Now, Pay Later (BNPL): A merchant's guide

Popular BNPL options: Klarna, Clearpay, Afterpay, and Atome.

4. Digital wallets

Digital wallets (or e-wallets) first appeared in the late 1990s, when they were mainly used to store card details for online payments. Over the years, they’ve developed into one of the most popular payment methods worldwide.

Broadly speaking, digital wallets typically come in two distinct forms.

- Pass-through wallets use existing card networks to process payments. They securely store a customer’s debit or credit card details and charge that card when the customer checks out. For example, when someone pays with Apple Pay, the transaction still runs through Visa or Mastercard: the wallet just makes it quicker and more secure.

- Stored-value wallets either hold pre-loaded funds that customers can top up, or they connect directly to a bank account. Payments are made straight from the wallet or bank, without going through card networks. For merchants, that can mean faster settlement times and lower fees.

Why should you offer digital wallets?

- Reduces friction during checkout, especially for mobile users. Thanks to pre-stored payment credentials and one-tap payments, merchants can decrease cart abandonment rates

- Decreases risk of fraud, as wallets often implement tokenisation, encryption, and two-factor authentication for enhanced security

- Enables cross-border transactions with multiple currencies, which helps merchants tap into global markets more easily

- Improves margins by lowering costs in some cases, especially where stored-value wallets are concerned

Popular digital wallets: Apple Pay, Google Pay, PayPal, Alipay, and WeChat Pay.

5. Digital cash-based payments

With cash-based online payments, customers can shop online, receive a voucher with a barcode or a reference number, and pay for it in cash at a participating store, retail outlet, or bank. Once this offline payment has been confirmed, the funds are transferred to the merchant.

This payment method is especially popular in markets with underbanked populations and low credit card penetration, such as Brazil (where Boleto Bancário is common – they have over 40,000 processing points in the country) or Mexico (where customers often use OXXO Pay).

This way, customers get to enjoy online commerce while still being able to rely on cash payments.

Why should you offer digital cash-based payments?

- Makes it easier to reach a broader customer base in markets where cards and digital wallets aren’t as prevalent

- Increases trust and conversion in markets where there’s a strong preference for cash

- Comes with low operational, fraud, and chargeback risk due to cash payments being confirmed as final at participating locations

Popular cash-based methods: Multibanco, PaySafeCard, OXXO, and Payshop.

Book a call with Primer to find out how we can help you integrate all of the payment methods above in just a few clicks

Why you need to offer diverse—not just more—payment methods

Simply adding as many payment methods as possible isn’t the solution. A cluttered list of options can overwhelm customers and actually damage the checkout experience. The goal isn’t volume; it’s strategic diversity.

A well-curated payment mix reflects your target markets and demographics. Younger shoppers often prefer mobile wallets and BNPL options, for example, while older generations tend to rely on credit and debit cards.

By understanding and responding to these patterns, you can provide customers with the right options at the right time, without overcomplicating the checkout process or adding unnecessary overhead.

Three tips for building the optimal payment method mix for your customers

1. Avoid choice overload: more isn’t always better

Our 2023 research finds that 15% of shoppers abandon a purchase if the checkout feels too complex. Being presented with too many payment choices means that the customer has to deliberately slow down, sort through both relevant and irrelevant payment options, and make a decision, all of which causes friction at a critical buying moment.

Then there’s the operational overhead on the merchant’s side of things. Managing too many accounts and integrations means that merchants must pour resources into building the necessary technical layers, as well as ongoing maintenance, compliance, and developing local customer knowledge.

Our advice is to choose enough payment methods to appeal to your target customers, but not so many that it causes confusion and cart abandonment.

2. Localize your payment methods to your target markets

Payment preferences vary widely by region, and getting them right is vital to unlocking conversion.

- Location matters most: While Dutch shoppers expect iDEAL, French customers trust Cartes Bancaires, and Mexican consumers rely on OXXO. Failing to offer these options can instantly block a sale.

- Demographics add another layer: For example, younger shoppers lean toward BNPL and wallets, and older segments stick to cards or PayPal.

- Customer behavior shapes priorities: Mobile-first shoppers in Southeast Asia might want to pay using digital wallets like TrueMoney or bank transfer options like PromptPay, whereas German customers often use PayPal for security and familiarity reasons.

By tailoring your payment options to regional and demographic expectations, you make checkout feel familiar and trustworthy, no matter where your customers are.

3. Balance processing costs and conversion through structured testing

Managing payment costs isn’t about guessing. It’s about testing what actually works. Some methods drive higher conversion but come with steep fees, while others are cheaper but may not perform as well with certain audiences. The smartest payment teams use real experiments to find the mix that maximizes both conversion and margins.

Take BNPL, for example. It can drive higher-order values and boost conversion, but the processing fees are often much higher than cards. But does that uplift actually offset the added cost? The only way to know is to test.

For instance, you could A/B test showing BNPL as the default option for first-time shoppers or for purchases over a certain basket size, and compare the results against a control group. This reveals whether BNPL truly lifts conversion and order value enough to justify the extra fees.

Structured experimentation turns payment strategy from guesswork into a measurable growth lever.

How Primer is making it easier to choose and integrate the right payment methods for your business

Imagine trying to assemble a picture with puzzle pieces from different sets. That’s what adding new payment methods before Primer was like: time-consuming, complicated, and with results that were short of optimal.

Each addition meant another lengthy integration, more custom routing logic, more reconciliation workflows, and another dashboard to keep track of. What should have been a simple way to boost conversion often turned into months of engineering work and ongoing operational overhead.

Primer was built to solve exactly this problem, and is trusted by leading ecommerce businesses like New Look, GetYourGuide, and Maisons du Monde.

It’s a unified payments infrastructure that lets merchants connect to multiple payment methods, payment processors, and other services through a single integration. Instead of building and maintaining separate connections for every new provider, you get one centralized layer to manage them all.

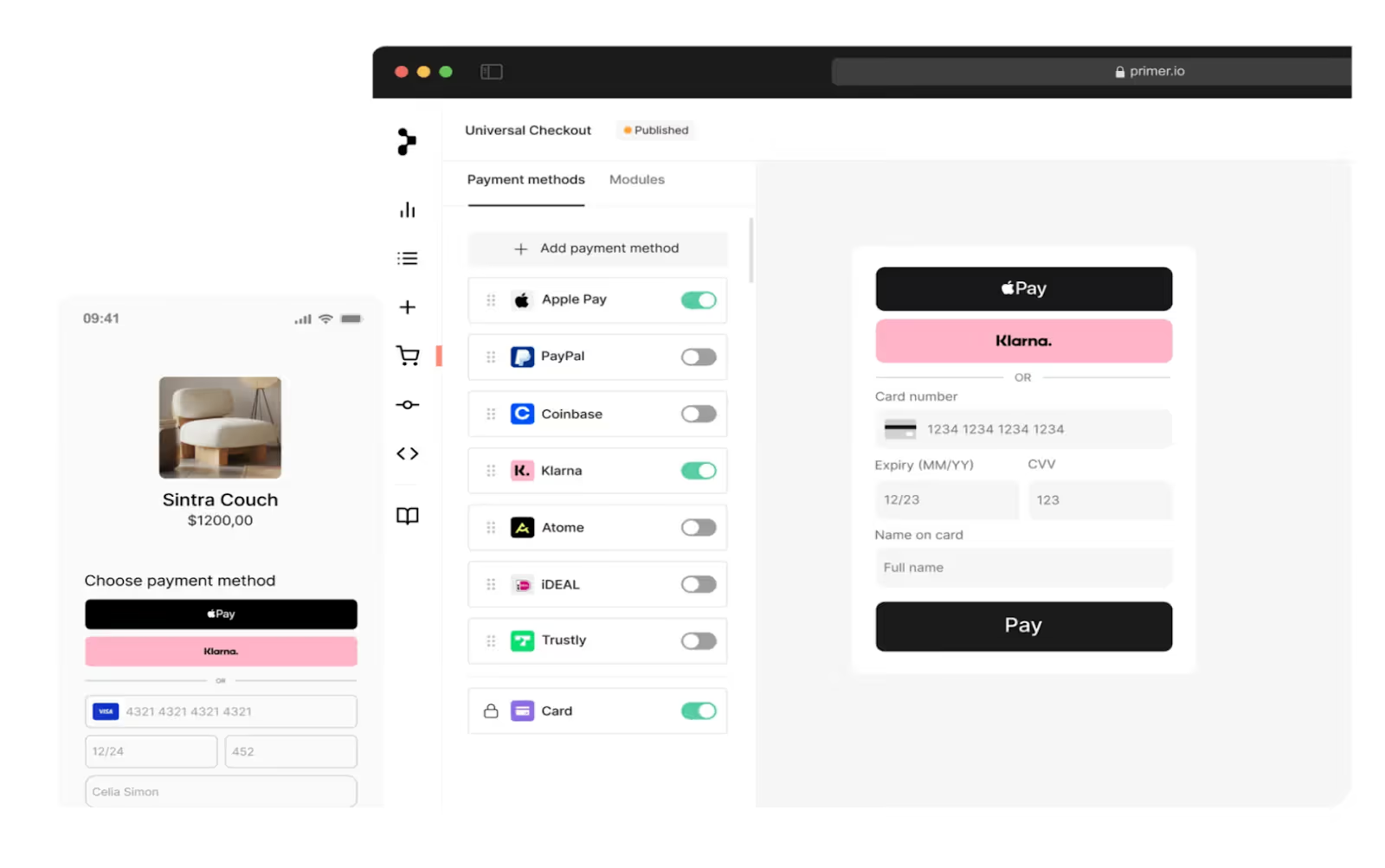

With Primer, you can add new payment methods in minutes without relying on engineering sprints.

Here’s what that looks like in practice:

Add new payment methods quickly – no code required

Primer enables you to:

- Activate 100+ payment methods through a single integration, from Apple Pay and Google Pay to iDEAL, Klarna, Sofort, Trustly, and PayPal

- Turn on new payment methods instantly once you’ve picked your preferred gateway and linked your merchant account

- Customize your checkout by region, device, or cart type in just a few clicks

Compare payment method performance to improve margins and drive conversions

Integrating payment methods in-house means that all your data is scattered across many accounts. As a result, figuring out which methods work best in your target markets can be frustrating.

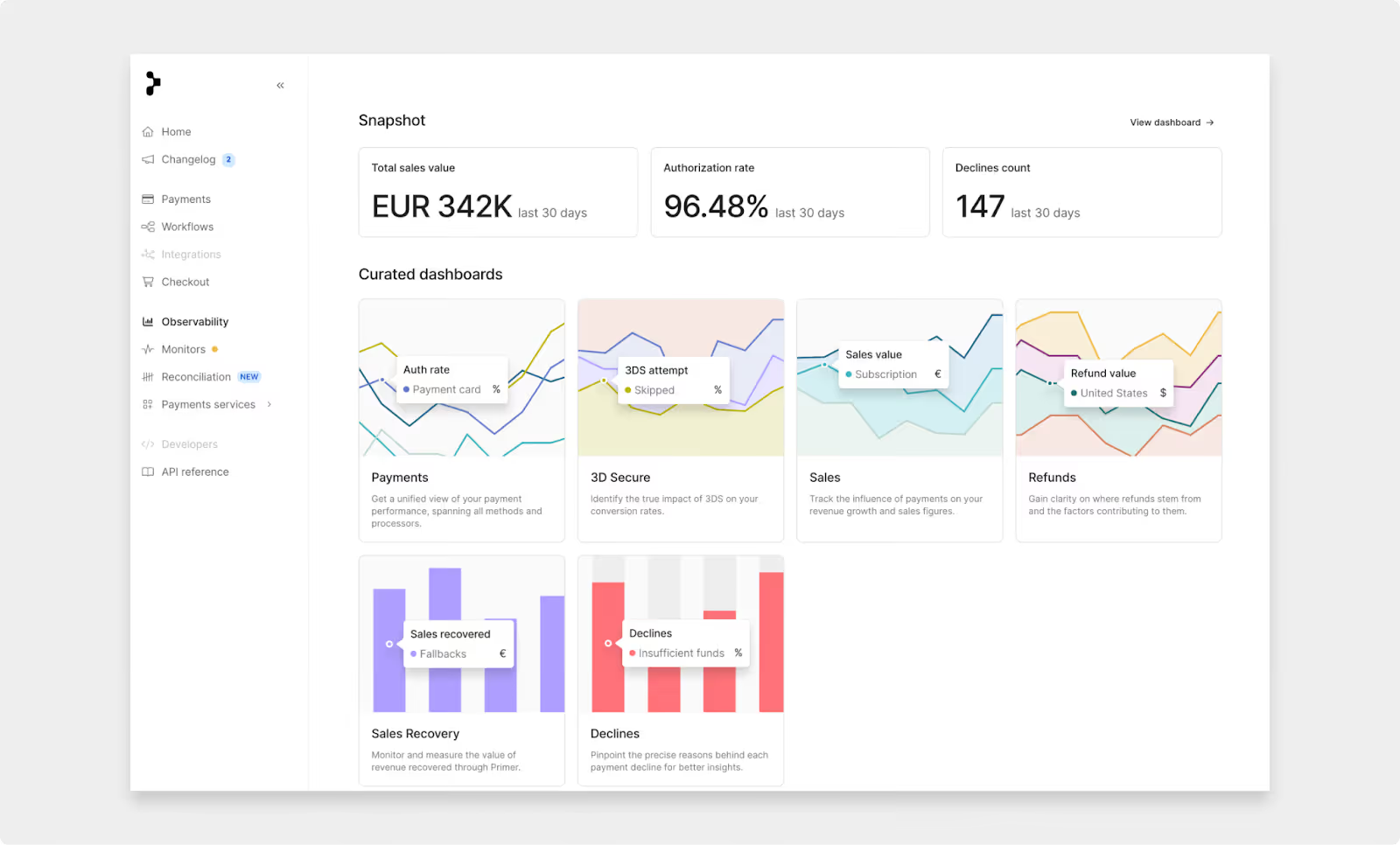

Primer’s Observability Dashboard makes it easy to see the full picture.

You can view all your data across payment methods in one place, with standardized formats and statistics that make it easier to slice and compare your payment routes based on authorization rates, currency, geography, and other factors.

You can also make use of Primer’s Monitors, which enable you to set up real-time notifications for certain payment trends.

For example, you might create a rule to alert your team if payment acceptance rates for a specific PSP drop below a certain threshold, or if declines increase sharply in a key market. That way, you can identify issues early and switch routes before they affect sales.

Recover lost revenue seamlessly with Fallbacks

Customers expect frictionless checkout. If they fail due to a soft decline and the transaction doesn’t go through, they might abandon the cart, leaving you with a lost sale.

Fallbacks help you recover those soft declined payments by automatically routing failed transactions to a secondary method, with no intervention on the customer’s end. To them, checkout is as seamless as ever. To you, a failed payment turns into recovered revenue.

Take Banxa, a leading crypto infrastructure that has managed to recover +17% of qualifying payments using Primer’s Fallbacks. Just in the first half of 2024, this meant over US$7 million that could have slipped away.

And because Primer offers agnostic 3DS, your customers don’t need to re-authenticate each time we route a transaction to a fallback method.

This way, you get to minimize checkout friction, increase potential sales, and configure your own specific payment strategy with the right tools at your disposal.

Offer the best mix of ecommerce payment methods at checkout with Primer

Offering a variety of checkout options to customers is beneficial, but a profitable payment strategy goes a step further than that.

From targeting the right customers in the right regions to testing how different payment methods fare when it comes to costs, settlement speed, and authorization rates, there’s a lot to choosing the best payment methods for ecommerce.

With Primer, you get to optimize this process by adding new payment methods quickly, slicing your data based on different metrics to determine optimal payment routes, and creating payment flows based on custom logic to enhance the customer experience.

Book a call with our team to learn more about improving your checkout strategy.

FAQs: Best payment methods for ecommerce

1. What are the most popular payment methods for ecommerce?

The most popular online payment methods for ecommerce businesses include credit and debit cards, as well as digital wallets like PayPal, Apple Pay, and Google Pay. Account-to-account (A2A) payments are common in countries such as the UK or Thailand, while cash-based online payment systems are a preferred choice in regions like Latin America. Many ecommerce platforms also integrate Stripe or other payment providers to handle secure payments and offer a smoother checkout experience.

2. How do I decide which payment methods to offer in my checkout?

When deciding which payment solutions to support, consider factors such as customer location, device preferences, and average order value. An ecommerce store targeting mobile-first customers should prioritize mobile payments and digital wallets, while a small business selling higher-priced products could benefit from offering BNPL options. The key is to match your customer preferences with the payment functionality that drives the most conversions.

3. How do payment methods affect my profits as a merchant?

The right mix of payment systems directly impacts your bottom line. Offering flexible online payment methods can reduce cart abandonment and boost conversions, while certain payment processing options come with higher monthly fees or risk exposure. For instance, BNPL and credit cards often carry higher fees but provide strong fraud protection and higher conversion potential. Meanwhile, A2A payments and direct debits typically offer lower costs and faster international payments.

4. How can I easily and quickly integrate multiple payment methods?

Platforms like Primer streamline the process for ecommerce sites by enabling merchants to integrate many payment methods, including Stripe, Shopify Payments, and multi-currency options, with just a few clicks. There’s no need for custom plugins or complex development. Primer also helps online businesses monitor performance, compare payment providers, and optimize their setup for fraud detection and reliability.

5. Are local payment methods better than international cards?

Local payment systems often provide faster settlement, lower fees, and stronger fraud prevention, while international cards like Visa or Mastercard support global reach. Ideally, ecommerce websites should offer both to maximize customer satisfaction. Letting shoppers pay in their preferred local method, whether through domestic card schemes, mobile payments, or online payment systems, builds trust and helps startups and small businesses grow more efficiently.

6. How do I make sure my ecommerce payment system is secure and PCI DSS compliant?

Security is a critical part of any ecommerce payment system. To process online transactions safely, merchants must comply with PCI DSS (Payment Card Industry Data Security Standard), a global framework designed to protect payment information and reduce fraud risk.

Platforms like Primer simplify secure payment management by ensuring all integrated payment providers meet PCI DSS standards. Primer also helps merchants improve fraud detection and fraud prevention by unifying data from every payment solution, giving you a single, real-time view of your checkout performance and security health.

.png)

.avif)