At first glance, the payment ecosystem in Australia looks pretty straightforward.

But dig deeper, and the Australia payment methods: What you need to offer your customerspicture changes. Australians are among the world’s fastest adopters of digital wallets. BNPL has exploded, with players like Afterpay and ZIP becoming household names. Real-time payments through the New Payments Platform (NPP) are also reshaping how money moves. Some merchants are even testing cryptocurrency to attract younger demographics.

The challenge is understanding how your customers want to pay and offering a payment mix that meets their needs. But even once you’ve identified the right methods, integration often becomes the roadblock.

Adding new payment options can quickly drain engineering time. And once live, you’re left juggling multiple dashboards and inconsistent data.

In this guide, we’ll walk through the essential Australian payment methods, the hurdles merchants face when adopting them, and how you can build a payment stack that scales without slowing down your business.

Want to offer additional payment methods to your customers without the engineering headache? Get in touch with Primer.

Which Australian payment methods should all online merchants offer?

Australia is moving fast toward a cashless society. By 2022, only 13% of payments were made with cash. In 2023, Australians were cited as among the least likely in the world to use cash at all.

With widespread ATM closures and rapidly changing consumer habits, some analysts project the country will go fully cashless within the next 30 years.

For merchants expanding into Australia or optimizing their local flows, enabling the right mix of payment methods is key to staying competitive and driving conversions. Here’s a closer look at how Australians prefer to pay today.

Credit and debit cards

Australians are gradually changing the way they use their cards to pay. Debit cards are steadily overtaking credit cards, with the number of active credit cards continuing to decline.

Visa and Mastercard remain the most widely used card schemes, but Australia also has its own local debit system, eftpos (Electronic Funds Transfer at Point of Sale). Eftpos transactions now make up about 35% of all online debit card payments, and merchant fees are roughly 40% lower on average compared to Visa or Mastercard.

Most eftpos cards today are co-branded with Visa or Mastercard, which means merchants can typically accept them without a direct eftpos integration.

Digital wallets

Around 46% of Australian debit cards and 40% of credit and charge cards are enrolled in at least one digital wallet, and usage will only grow. The market for digital wallets is projected to grow 9.9% annually, to reach $35.71 billion by 2029.

The most widely used wallet is Apple Pay, which makes up more than half of all mobile payments. It’s followed closely by Google Pay and Samsung Pay.

Other digital wallets commonly used in Australia include:

- AliPay

- Amazon Pay

- Beem it (eftpos)

- PayPal

- WeChat Pay

BNPL

Buy Now, Pay Later (BNPL) lets customers pay in installments over a set period of time, often with no interest or fees. It’s becoming a baseline expectation for online shoppers, especially among Gen Z and Millennials.

In 2024, the BNPL adoption rate in Australia was the highest in the world, with 2.5% of customers having used it to pay for their most recent ecommerce purchase. That’s in comparison with around 1% in most countries, and only 0.9% in the U.S.

The most common BNPL setup is one upfront payment followed by three biweekly payments. Some providers also offer longer-term plans (up to 24 months), which may or may not include interest depending on the terms.

In Australia, the most popular BNPL methods include:

- Global providers: Afterpay and Klarna

- Local alternatives: Humm and Payright

Under new regulations, these and other BNPL providers will need to meet the same standards as other credit providers, including:

- Hold an appropriate license

- Be approved by ASIC

- Become a member of the Australian Financial Complaints Authority (AFCA)

They will also be subject to new lending rules, disclosure standards, and price controls.

Real-time payments

Real-time payments, also known as “Pay by Bank,” are a fast-growing account-to-account (A2A) payment method in Australia. Common methods include:

- PayTo

- PayID

- Osko by BPAY

The latter two are mainly used for peer-to-peer and in-person transactions like market stall payments, although PayID adoption is increasing among other businesses.

All of these services are powered by the New Payments Platform (NPP), an open access infrastructure for making fast payments in Australia. Launched in 2018, NPP facilitates around $5 billion in payments a day across 100+ Australian banks, fintechs, and other financial institutions.

Most real-time payments in Australia work the same way: the merchant sends a payment request to the customer via SMS, email, or app. Once the customer authorizes the agreement, funds are transferred instantly and directly from the customer’s bank account to the merchant.

Read more about real-time and account-to-account payments: Spotlight: Open Banking

Cryptocurrency

In 2025, 31% of Australians said they owned or had owned crypto, up from about 25% in 2022.

Meanwhile, the Commonwealth Bank of Australia (CBA) has announced plans to add crypto services to its app, and NAB (The National Australia Bank) has launched its own AUDN stablecoin.

Many companies are now accepting crypto payments for essential services like electricity and internet. Australian Bitcoin holders can even use crypto as collateral for home loans.

But just because Australians have cryptocurrency and some businesses accept it doesn’t mean anyone is actually using crypto to transact.

In 2023, a Reserve Bank of Australia study found that fewer than 2% of respondents had used cryptocurrency to make a payment in the past year. That same study suggests that high transaction fees and limited merchant acceptance may be to blame.

Given such low usage, it’s understandable that merchants might be hesitant to accept crypto. That’s because:

- It’s complex: Setting up wallets, securing keys, and managing risk requires in-house expertise.

- It’s hard to integrate: Without orchestration, adding crypto to your stack often needs custom development.

- It’s risky: Payments are irreversible, and you’ll need to build your own refund processes.

- It’s volatile: Prices swing rapidly, and regulations are unpredictable.

So, should you accept crypto? That depends. For many businesses, the risks and costs simply aren’t worth it. But for niche, tech-forward businesses, accepting crypto can attract exactly the right audiences.

To learn more about offering customers different ways to pay, read our Ultimate Guide to Alternative Payment Methods.

How to integrate payment methods in Australia

Many merchants add new payment methods by integrating directly with a payment gateway, using their API or SDK to get started.

But there are a few major downsides to this approach:

- You can only use the payment methods your gateway supports. As you expand into new markets, you’ll need the flexibility to offer local A2A, digital wallet, and Buy Now Pay Later (BNPL) options. But a single gateway might not offer all the methods you want in each region, so you’ll have to integrate with multiple gateways just to cover your bases.

- Every integration is a custom project. Your developers have to build and maintain each connection with each new payment method, which can mean delays, dev tickets, and opportunity costs.

- You lose control of the checkout experience. Some gateways force you to use their default logic or UI, limiting your ability to optimize for conversions or create the brand experience you want.

- Even minor updates can mean more developer work. A new payment method can take months to integrate and launch, but a single provider update days later can send your team right back into the code.

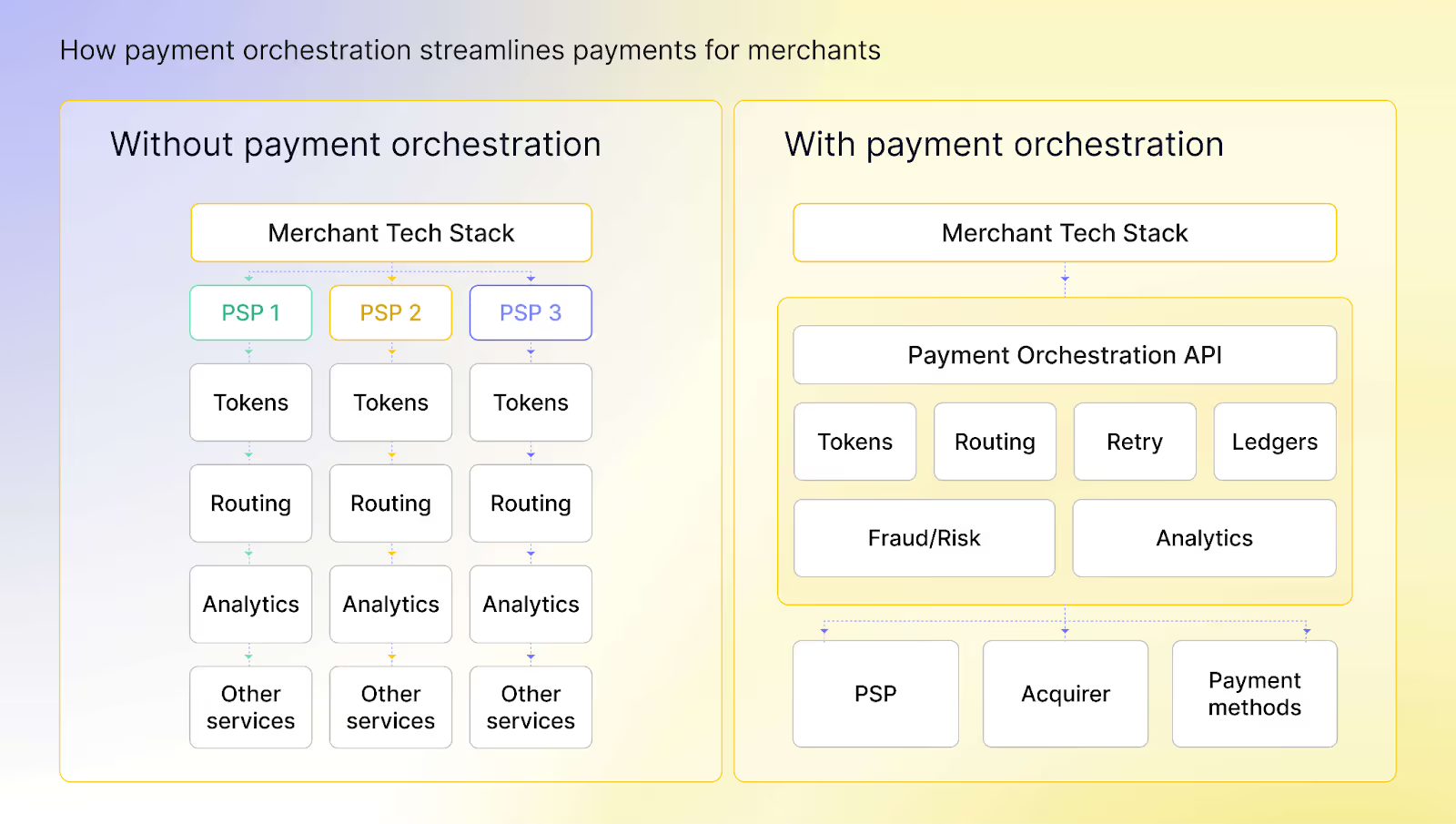

Fortunately, there’s a faster, more flexible way to manage payment methods: payment orchestration.

Read more: Multiple payment methods: Everything you need to know

What is payment orchestration and how can it help?

Payment orchestration consolidates all your integrations with different payment methods, providers, and services. Instead of building and maintaining multiple direct integrations, orchestration lets you scale and manage your entire payment system all in one place.

A payment orchestration platform (POP) lets you use custom logic to route transactions across different payment services. It’s a control center for all your payment operations.

Read more: What is payment orchestration and how can it maximize payment efficiency?

How Primer makes it easy to add, test, and update new Australian payment methods

Every new market brings the same payments puzzle. In Australia, that might mean adding ZipPay, PayTo, or Apple Pay, each one a separate project, each one draining weeks of engineering time. You end up with a checkout stitched together from half a dozen integrations and a data trail scattered across as many dashboards. Scaling stops feeling like growth and starts feeling like maintenance.

Primer was built to flip that script.

With one integration, you unlock a Unified Payment Infrastructure that connects every method and service you need. And unlike traditional orchestration, which stops at routing, Primer gives you control of the entire payment experience. A flexible checkout you can adapt instantly. A no-code workflow engine to test and automate logic. Data you can actually act on, all in one place.

Instead of wrestling with payments, your team can finally treat them as they should be: a lever for growth, not a barrier.

Here’s how Primer makes it simple to activate new payment methods as you scale into Australia:

Add and manage new global and local payment methods without the technical lift

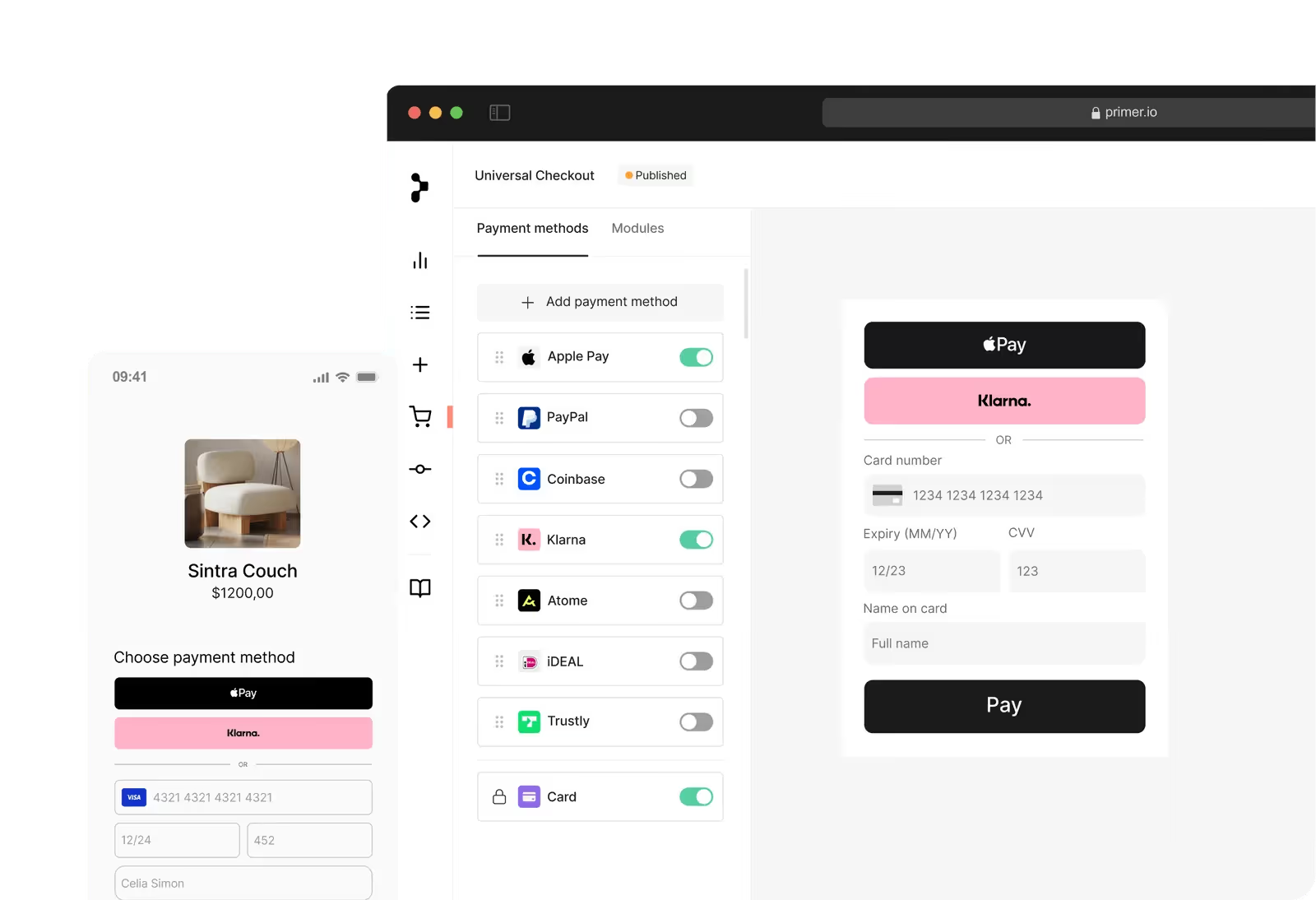

Adding a new payment method with Primer is easy. It only takes two steps:

- Head to Integrations in the Primer dashboard and activate the payment method

- Use Universal Checkout to manage how that payment method is displayed at checkout

Once you’ve activated a payment method, you don’t need engineers to keep it running smoothly. We handle all updates and maintenance in the background.

With Primer, you can activate a wide range of popular payment methods, including:

- Afterpay

- ApplePay

- PayPal

- Google Pay

- Klarna

As well as APAC payment methods relevant to many Australian consumers, such as:

- AliPay

- PayNow

- Shopback

- ShopeePay

- WeChat Pay

We’re also constantly adding new payment methods, but if you don’t see one you want, you can request it via the Primer Dashboard or reach out directly to our support team.

Read more: Alternative payment methods: offer customers more ways to pay.

Localize the user experience with a no-code checkout builder

In Australia, cart abandonment rates at checkout may be as high as 88%. One of the most effective ways to reduce that number is to offer a smooth, simple checkout experience.

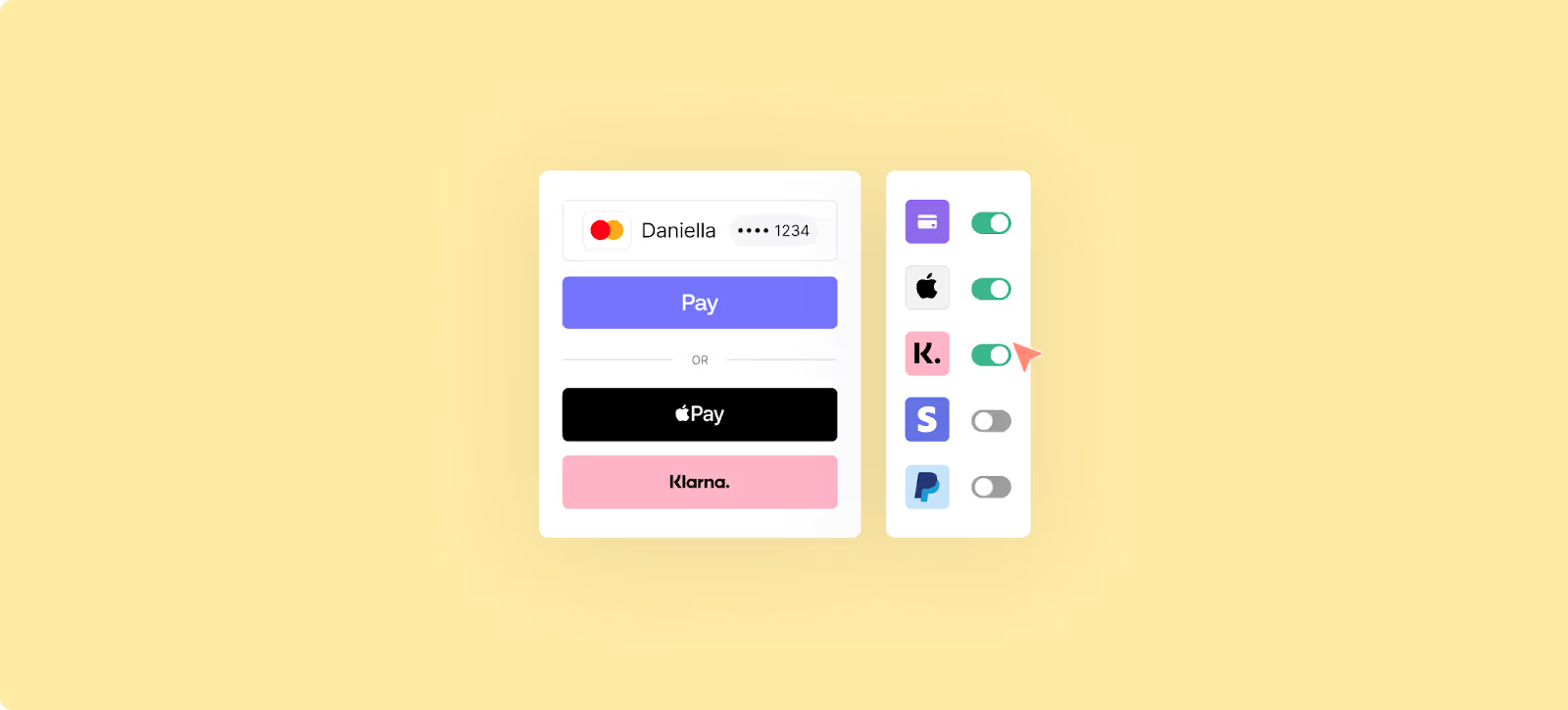

Primer’s checkout builder lets you refine and personalize checkout flows, so customers see only the most relevant payment methods.

Once you’ve activated all the payment methods you want, it’s easy to:

- Add, reorder, or remove payment methods in seconds

- Set up different checkout flows for different customers based on their region, device type, or customer details

- Instantly respond to issues like a temporary ApplePay outage or changing regulations around crypto or BNPL

You can also customize the look and feel of your checkout with colors, fonts, button text, and other styling elements. With Primer, you’re never limited to dull templates, generic text, or clashing color schemes.

In short, Primer's checkout builderempowers your team to take control of your checkout strategy, so you can optimize for conversions, build a better user experience, and flexibly adjust as you go.

Read more: Set up your checkout with clicks, not code

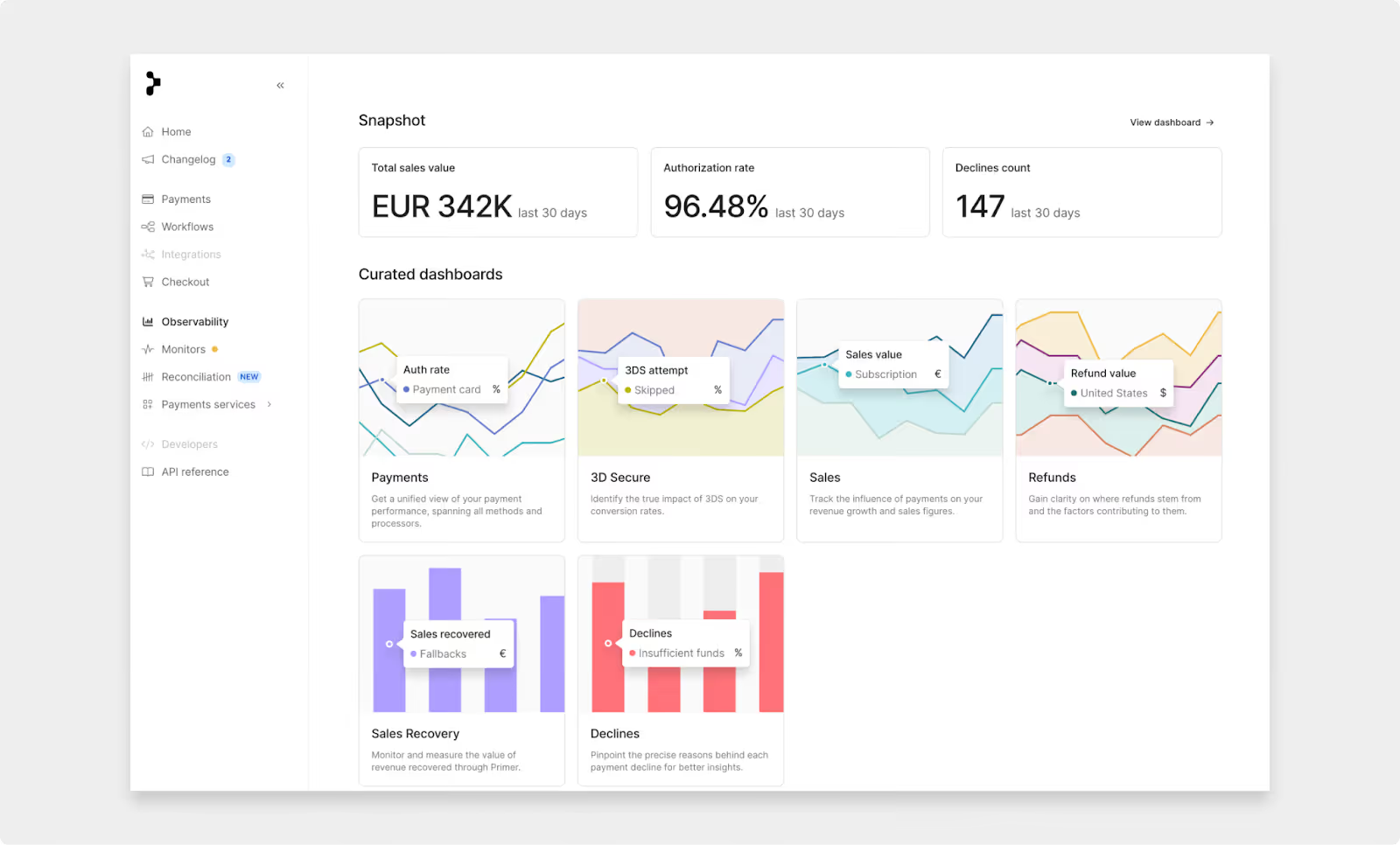

Get a unified view of all of your payment data with Observability

Launching a new payment method or tweaking checkout is only half the battle.

The other half is working out whether it actually made a difference. Without visibility, you’re left guessing whether a new option boosted conversions, hurt performance, or introduced hidden costs.

Instead of juggling spreadsheets and fragmented dashboards, Primer Observability gives you a single source of truth for your entire payment stack. You can see, in real time, how each method, flow, or provider is performing, and quickly spot where revenue is being won or lost.

With over a hundred visualizations and filters, Observability lets you drill into the details that matter: Which payment methods are driving conversions? Where are declines spiking? How do fraud checks or 3DS flows affect authorization rates?

The result is clarity. Instead of guessing, you can test, measure, and refine your payment strategy with confidence, and scale knowing precisely what’s working.

How Dabble is future-proofing its Australia payment stack with Primer

To compete in Australia's saturated and tightly regulated betting market, social betting app Dabble needed to offer more payment methods, like Apple Pay and Google Pay. Convenience and performance are critical to their business, especially during peak periods: customers will drop off quickly and permanently if they can’t place their bets.

But manual integrations were slowing down their time to market and consuming developer resources. Spending weeks or months building complex integrations wasn’t an option.

With Primer, Dabble was able to:

- Instantly activate Apple Pay and Google Pay without developer lift

- Onboard multiple payment processors at once to build redundancy and boost performance

- Build processor redundancy and prevent payment failures during peak periods

- Use real-time fraud alerts to stay on top of payment failures and processor outages

Without the need to rebuild payment logic every time they update their payment stack, Dabble has the flexibility to adapt quickly. They can focus on scaling to new regions, easily adding payment methods and processors as they go.

Read the full case study here: Dabble picks a winner by partnering with Primer

Offer the payment methods your customers expect with Primer

Expanding into Australia, or optimizing your payments for the region, doesn’t need to mean weeks of engineering, clunky integration, or guesswork around what’s working.

With Primer, you can quickly activate relevant local and global payment methods, customize your checkout experience, and analyze your payment stack, all without any code.

Book a call to add Australian payment methods faster, with Primer.

FAQ Picking the right payment methods in Australia

What are the most popular payment methods in Australia?

Australians use a mix of debit and credit cards, eftpos, digital wallets like Apple Pay and Google Pay, BNPL services such as Afterpay, and account-to-account payments through PayTo and PayID. Primer helps merchants activate these methods quickly through a single integration.

How do digital wallets impact ecommerce in Australia?

Digital wallets like Apple Pay, Google Pay, and PayPal are widely adopted and growing fast. They improve conversion by making checkout smoother. Primer enables merchants to add and manage these wallets without extra engineering effort.

Why is BNPL so important in Australia?

Australia has the highest BNPL adoption rate in the world, led by providers such as Afterpay and Zip. Offering BNPL can boost conversions, especially among younger shoppers. Primer makes it simple to activate BNPL options alongside other methods.

What role does the New Payments Platform (NPP) play?

The NPP powers real-time account-to-account payments in Australia, including PayTo, PayID, and Osko. Merchants can use these methods to reduce costs and improve speed. With Primer, these A2A methods can be activated and managed in one place.

How can merchants add multiple payment methods in Australia?

Direct integrations with gateways can be slow and costly. Primer offers a unified payment infrastructure, letting merchants activate and test Australian methods like eftpos, BNPL, and digital wallets without heavy development work.

.png)

.avif)