Travel merchants can reduce payment fees and cross-border costs by combining local acquiring, multi-currency capabilities, alternative payment methods, and payment orchestration platforms like Primer to optimize how transactions are processed globally.

There is no single solution that solves this problem on its own. High payment costs usually come from a mix of FX fees, cross-border card charges, poor routing decisions, and reliance on a single provider. The most effective approach is to combine the right solutions and use a platform like Primer to control how they work together.

Where cross-border payment costs come from

Before looking at solutions, it helps to understand the main cost drivers:

- Cross-border card fees when issuer and acquirer are in different regions

- FX conversion markups

- Intermediary banking fees

- Low authorization rates leading to lost revenue

- Inefficient routing to higher-cost PSPs

Reducing costs is not just about finding cheaper providers: it’s also about processing payments more intelligently.

The key payment solutions travel merchants use

Local acquiring and multi-currency setup

One of the most effective ways to reduce costs is to process payments locally.

This means:

- Routing transactions to local acquirers

- Accepting payments in local currencies

- Settling funds without unnecessary conversions

Local acquiring reduces cross-border fees and often improves authorization rates at the same time.

Alternative and local payment methods

Relying only on international card networks can be expensive.

Travel merchants increasingly support:

- Local bank transfer methods such as iDEAL and SEPA

- Digital wallets like Apple Pay, Google Pay, and PayPal

- Region-specific methods such as Alipay

These methods can reduce costs by avoiding cross-border card fees, using domestic payment rails, and increasing conversion rates.

Read more: Alternative payment methods: offer customers more ways to pay

Cross-border and FX-optimized providers

Some providers specialize in reducing FX and international transfer costs by:

- Offering multi-currency wallets

- Providing more competitive exchange rates

- Using local settlement infrastructure

These are often used alongside PSPs to improve treasury and settlement efficiency.

Read more: How to reduce FX fees for businesses

Virtual cards and payout solutions

For OTAs handling supplier payouts, virtual cards and local payout rails can:

- Reduce FX exposure

- Improve reconciliation

- Lower operational overhead

This is especially important in travel, where payments flow both inbound from customers and outbound to suppliers.

Why payment orchestration using Primer is key to reducing costs

While all of the above solutions help, the biggest cost savings often come from how payments are routed.

This is where Primer plays a central role.

Instead of relying on a single PSP or a static setup, Primer allows travel merchants to:

- Route transactions to lower-cost providers based on region or payment type

- Use local acquirers automatically where available

- Optimize for authorization rates and cost at the same time

- Avoid unnecessary cross-border processing

- Test and adjust routing strategies over time

Primer doesn’t replace these solutions: it helps them work together more efficiently.

For instance, a travel merchant using multiple PSPs might process all transactions through one provider, even when better or cheaper options exist.

But with Primer, that same merchant can:

- Route European transactions to EU acquirers

- Send high-value bookings through more reliable processors

- Use alternative payment methods where card fees are higher

- Avoid routing transactions across borders when it is not necessary

Over time, this reduces both direct processing costs and indirect costs from failed payments.

Reduce FX fees and stay on top of payment costs with Primer

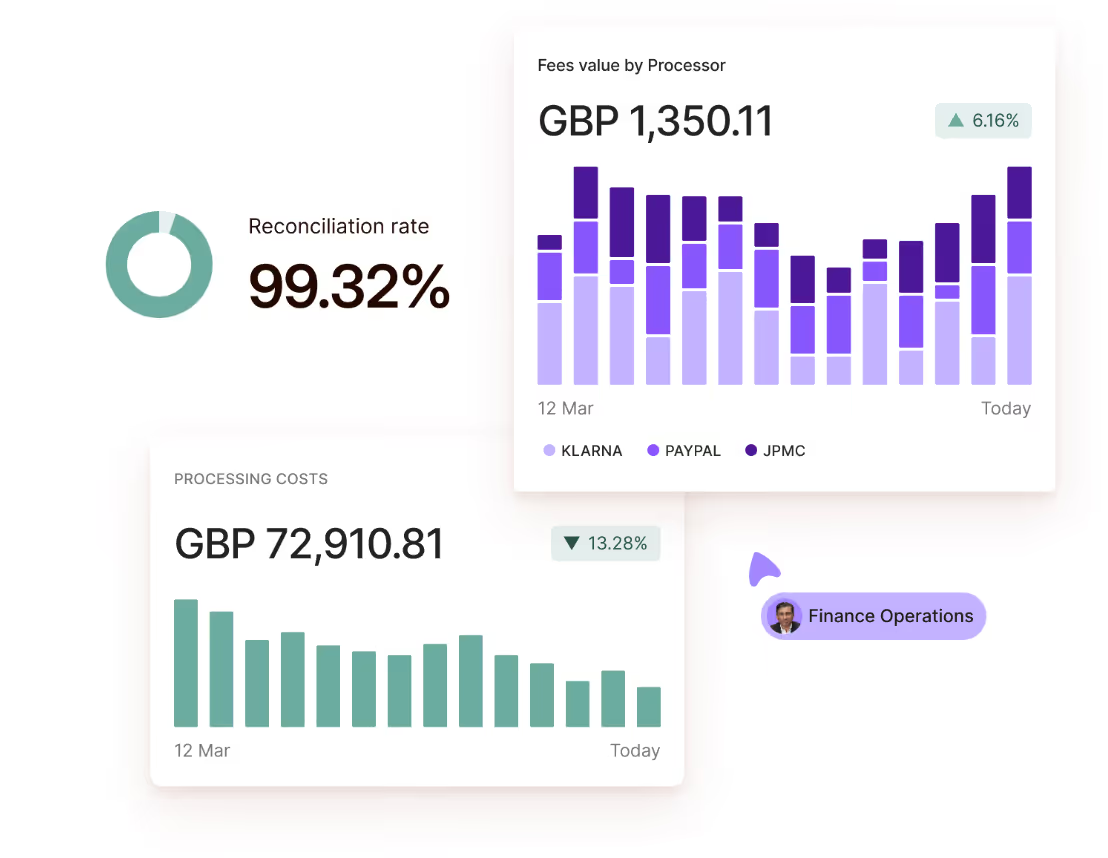

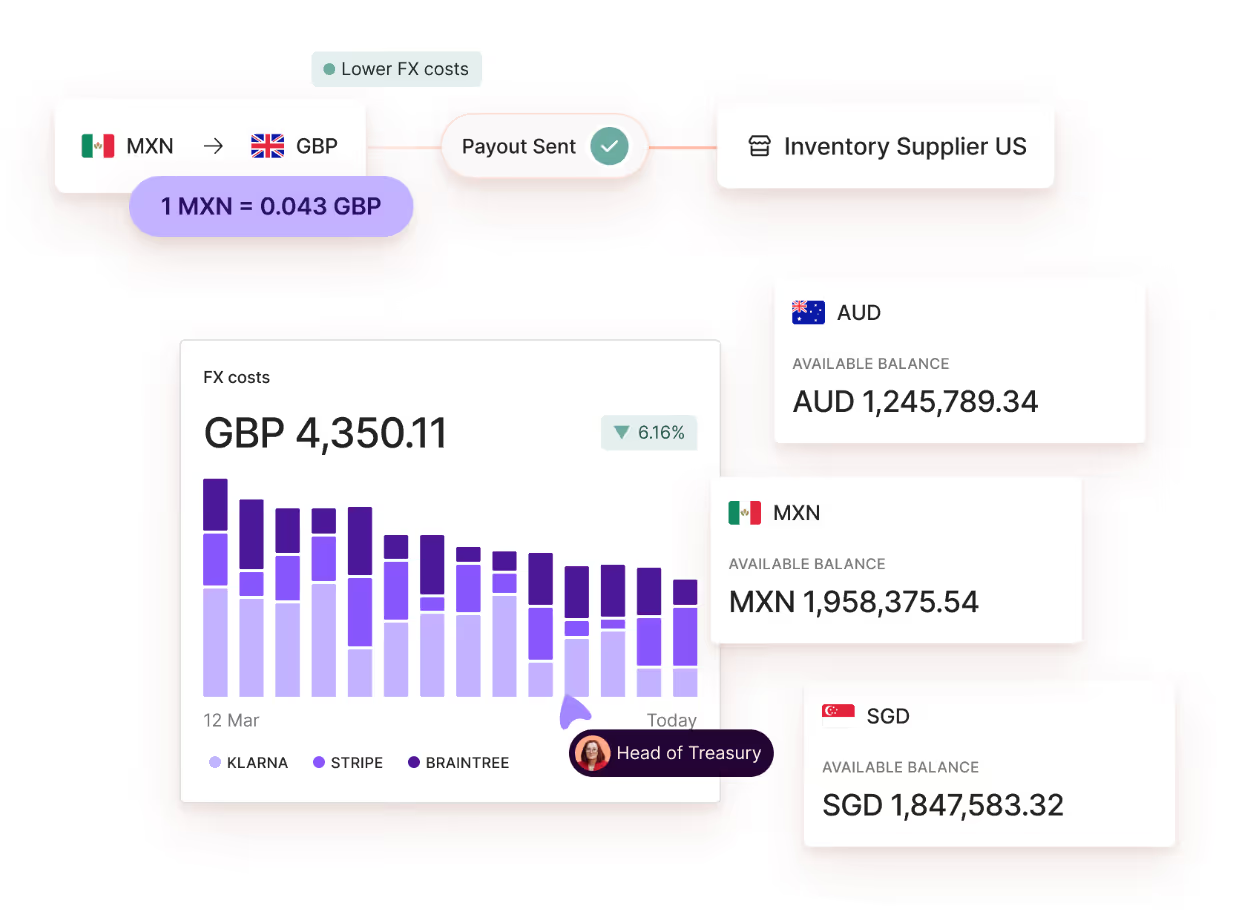

Travel merchants need clear visibility into what they are actually being charged across PSPs and currencies. Primer provides this through Costs Overview and Global Accounts, giving teams both transparency and control.

Costs Overview standardizes fees across all providers into a single structure, including

interchange, scheme, processor, and FX costs. This makes it easier to compare PSPs, understand true cost per transaction, and identify where fees are higher than expected.

And with Global Accounts, merchants can collect payments locally, hold balances in multiple currencies, and control when conversions happen. This reduces unnecessary FX fees and avoids repeated currency conversions.

Together, these capabilities allow travel merchants to route payments based on both cost and performance, benchmark providers, and reduce cross-border cost leakage over time.

Want to see how it works for yourself? Book a demo with Primer.

Frequently Asked Questions (FAQ): Payment solutions that help travel merchants reduce payment fees

What is the biggest driver of cross-border payment costs?

Cross-border card fees and FX markups are typically the largest contributors, especially when transactions are processed outside the customer’s region.

Do local payment methods reduce fees?

Yes. Local payment methods often use domestic payment rails, which can reduce fees and improve authorization rates.

How does Primer help reduce payment costs?

Primer enables smart routing across PSPs and payment methods, allowing merchants to process transactions through the most cost-effective and high-performing options.

Is using multiple PSPs enough to reduce costs?

Not on its own. Without orchestration, merchants cannot control how transactions are routed, which limits cost optimization.

.avif)