If you’re researching dynamic 3D Secure (3DS), there’s a good chance you’re experiencing the following:

- You want to reduce checkout friction while maintaining compliance with regulatory requirements.

- You need a 3DS strategy that allows you to set rules and conditions for triggering challenges, helping to reduce fraud and shift liability to issuers.

- You’re searching for a way to implement 3DS independently of payment processors, giving you the flexibility to create custom workflows and enable smoother customer retries.

Most merchants rely on their payment processor’s built-in 3DS solution. While convenient, this approach can limit your ability to implement a tailored strategy and deliver an optimal payment experience for your customers. That’s where a dynamic 3DS strategy can make all the difference.

In this article, we’ll explain how dynamic 3DS works, when it’s the right solution, and how Primer’s agnostic 3DS solution can help. Here’s what we’ll cover:

- What is a dynamic 3DS strategy?

- What are the benefits of a dynamic 3DS approach?

- How do you deploy a dynamic 3DS strategy with Primer?

- How Kilo Health used Primer 3DS to reduce fraud risk

If you are a company working to implement a dynamic 3DS strategy, contact us today to see how Primer can help.

What is a dynamic 3DS strategy?

When it comes to implementing 3DS, merchants can typically take one of two approaches:

- Apply 3DS to every transaction: Ensures compliance and liability protection but risks increasing cart abandonment due to added friction.

- Apply 3DS to only certain transactions: Uses pre-set rules and conditions to trigger authentication only when necessary, balancing compliance and customer experience.

A dynamic 3DS strategy takes this a step further, allowing merchants to enable 3DS authentication only when required by the issuer or when it aligns with their specific fraud prevention goals—such as for high-value transactions or risky markets.

Given that there is no one-size-fits-all approach to 3DS. Enabling it for every transaction may deter customers while restricting it to high-value transactions alone might leave vulnerabilities in your fraud prevention strategy.

Therefore, the most effective 3DS strategy is dynamic and considers your business’s unique risk tolerance, striking the right balance between reducing customer friction and ensuring robust fraud protection.

Learn more about creating a 3DS strategy: Key questions to ask when building an optimal 3DS strategy.

What are the benefits of a dynamic 3DS approach?

Here’s how dynamic 3DS can better balance security and customer experience.

Reduce check-out friction for European customers and limit abandoned carts

Customers expect fast, seamless transactions when making payments. Too much friction—like a clunky authentication process—can discourage customers from completing their purchases, resulting in lost revenue.

In fact, according to Baymard Institute research, 22% of people said they have abandoned carts during checkout in the last three months due to a complicated checkout process.

A dynamic 3DS strategy tailored to your business goals can help reduce this friction and improve the customer experience.

For instance, within the European Economic Area (EEA) and the UK, PSD2 regulations mandate authentication for transactions using 3D Secure. However, merchants can leverage exemptions to avoid unnecessary 3DS prompts in certain cases. These exemptions depend on factors such as the acquirer’s country, whether the transaction is recurring, or the merchant’s fraud rating through Transaction Risk Analysis (TRA).

By adopting a dynamic 3DS strategy, merchants can fully comply with PSD2 while strategically minimizing unnecessary friction, reducing cart abandonment, and optimizing conversions.

To learn more about SCA exemptions, read the following blog post: Complete Guide to SCA Exemptions.

Shift fraud liability and minimize fraud

A dynamic 3DS strategy gives merchants control over when to trigger authentication, allowing them to shift liability to the issuing bank in certain situations.

When 3DS is used, and the customer successfully authenticates, any fraud-related chargebacks become the issuer’s responsibility. This is why the key to an effective 3DS strategy involves carefully balancing the benefits of reduced friction from skipping authentication with the potential financial risk of retaining fraud liability.

For example, an eCommerce homeware retailer could use a dynamic 3DS strategy to trigger authentication only for purchases above €300. For a €30 lamp, the merchant might apply for an exemption so the customer can complete the purchase without 3DS. However, for a €1,500 dining table set, the transaction would require 3DS authentication to ensure added security and liability protection.

This approach minimizes unnecessary steps for low-risk transactions while enhancing security for higher-value purchases, balancing customer convenience and fraud prevention.

How can merchants deploy a dynamic 3DS strategy with Primer?

Primer provides a unified payments infrastructure that empowers businesses to seamlessly accept, optimize, and manage payments across multiple services—all through a single payment API integration. By removing technical complexities, Primer enables businesses to scale faster and unlock growth opportunities without being limited by traditional payment technology constraints.

With our powerful Agnostic 3DS solution, merchants get complete control over the execution of their 3DS authentication and, thus, payment strategy.

Here are three benefits merchants get when working with Primer’s 3DS.

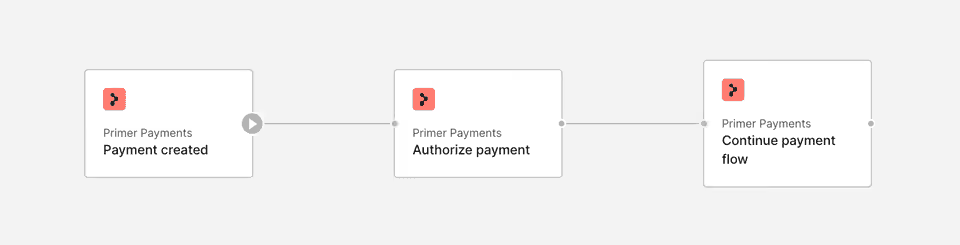

1. Optimize and customize your 3DS payment flows with Workflows and Adaptive and Agnostic 3DS

Most processors’ 3DS solutions don’t allow merchants to set custom conditions or logic—like “only trigger 3DS for online payments over €250 made with a Visa card.” Even if such functionality exists, it often requires manual setup for each processor, making it time-consuming and inefficient.

Primer has decoupled 3DS from any specific processor, simplifying its implementation across a merchant’s entire payment stack. Primer collects the challenge data during authentication and includes it in the authorization request sent to the processor.

With 3DS integrated into Primer’s Workflows tool, merchants can easily create and manage payment flows. Rules and conditions are set once and automatically applied across all processors, removing the hassle of configuring logic for each processor.

Merchants can route transactions based on virtually any condition they choose, such as custom metadata, card schemes, BIN numbers, or payment methods. This flexibility is supported across every processor that Primer integrates with, giving merchants unparalleled control over their 3DS strategy.

We’ve also pioneered a feature called Adaptive 3DS that allows merchants to trigger 3DS only when necessary, optimizing the balance between security and a seamless checkout experience with zero effort.

2. Use Agnostic 3DS to increase checkout conversion rates

Managing 3DS across multiple payment providers without an agnostic solution can quickly become overwhelming. Merchants must manually configure logic for each processor, and any changes require duplicating that effort across all processors—a cumbersome and error-prone process.

With Primer, that issue disappears. Merchants can centrally manage 3DS rules and logic through Primer’s platform, applying changes across all processors from a single dashboard. This eliminates the need for repetitive configurations, streamlines payment operations, and ensures a consistent, efficient approach to managing 3DS, no matter how many processors a merchant uses.

Additionally, Primer makes it much easier for merchants to establish a seamless fallback strategy. If a payment fails with one processor, Primer can reuse the original 3DS results and retry the transaction with another processor via our Fallbacks solution—all without requiring the customer to re-authenticate. This not only improves the customer experience but also reduces the likelihood of cart abandonment, helping merchants recover potentially lost sales.

3. Understand how 3DS impacts your checkout conversion rates and adapt your payment strategy accordingly

3DS processes generate a wealth of data in their authentication responses, but this information is often fragmented and difficult to interpret. Primer simplifies this complexity by aggregating and translating 3DS data through our Observability solution.

For example, while most platforms require merchants to interpret authentication responses using ECI codes, Primer provides a clear, straightforward answer: passed or not. We also highlight essential details like whether the transaction was frictionless or required customer interaction.

With Primer, merchants can answer critical questions such as:

- Did the customer see a pop-up, or was the authentication completed in the background with their bank?

- Was a request to explicitly challenge the customer passed?

- Is the transaction protected if a fraudulent chargeback occurs?

Additionally, merchants can access insights on what the 3DS authentication rate was across multiple metrics like card network, country, currency and more.

For CodesDirect, a Primer client who sells digital goods, the ability to spot problems and apply more aggressive authentication at the first sign of potential fraud for that issuer without writing code has been a game changer.

"No PSP to date has much control over 3DS. We’re now fully in control of how we process credit cards,” says Co-Founder Amrish Gayadien. “This means we can decide to force mandatory 3DS for certain countries or users with BINs. It’s sophisticated, and we can immediately adapt to a fraud attack and make changes to stop losing a lot of money."

How Kilo Health used Primer 3DS to reduce fraud risk

Kilo Health is a subscription business that supports four million customers globally. When Vytautas Šernas stepped into a Head of Payments role, the company knew they needed a central place to manage payments. This was especially true because they wanted more sensitive control over payment routing and 3DS checks across their global markets.

Other solutions promised a single payment integration but didn’t truly deliver that functionality. And the team quickly realized they couldn’t handle creating such a platform themselves. Enter Primer.

With Primer, Kilo Health could execute its 3DS strategy across its PSPs using our no-code Workflows tool. They used customer profiles to determine risk levels and avoid triggering 3DS with a low risk of fraudulent behavior.

That means customers who don’t need additional 3D Secure authentication aren’t burdened with extra steps, which has impacted Kilo Health’s revenue.

“We have a high ROI because we can have a higher risk tolerance as we now have the tools to manage it, vs. sticking with a single provider where we'd have to reduce our 'risk appetite' due to fewer tools to manage that. So, it's directly impacting our bottom line," explains Šernas.

Primer’s 3DS solutions enabled Kilo Health to completely control its risk appetite while meeting regulations and growing its business securely.

Learn more about how Kilo Health uses Primer.

Use Primer’s 3DS solution to improve payment experience and reduce fraud

Primer’s 3DS solutions provide your business with the flexibility needed to meet regulatory requirements and maximize the potential of 3DS. With smarter 3DS deployment, you can customize triggers based on your data, risk tolerance, and compliance needs—all while prioritizing a seamless customer experience and boosting conversions.

If you are ready to see how a unified payments infrastructure can improve your 3DS, contact Primer today.

Dynamic 3ds Frequently Asked Questions (FAQs)

What is a dynamic 3DS strategy?

A dynamic 3DS strategy allows merchants to apply 3D Secure only when it aligns with specific risk conditions or issuer requirements. Unlike static implementations, it enables the use of custom rules—like transaction value, card type, or region—to trigger authentication only when truly necessary. This approach helps reduce friction at checkout while still meeting compliance standards and fraud prevention goals.

How does dynamic 3DS help reduce checkout friction?

By selectively applying 3DS only when risk thresholds are met, merchants can minimize unnecessary challenges and provide a smoother checkout experience. For example, low-risk or recurring payments may qualify for exemptions under regulations like PSD2, which reduces cart abandonment and speeds up the customer journey.

Can dynamic 3DS reduce fraud liability?

Yes, when a customer completes 3DS authentication successfully, liability for any resulting fraud typically shifts to the issuing bank. A dynamic strategy allows merchants to trigger 3DS only for higher-risk transactions, balancing fraud mitigation and user convenience while protecting the business from chargeback costs.

What are the advantages of using Primer’s agnostic 3DS solution?

Primer’s agnostic 3DS tool decouples authentication from any specific processor, giving merchants full control over when and how 3DS is applied. This centralizes 3DS logic across all payment providers, simplifies changes, and enables advanced features like Adaptive 3DS, Workflows for rules-based routing, and fallback strategies that reuse 3DS results without requiring re-authentication.

How can businesses measure the impact of 3DS on performance?

Businesses can assess the performance of their 3DS strategy by analyzing metrics such as authentication success rates, frictionless vs. challenged transactions, conversion rates post-authentication, and chargeback outcomes. Tools like Primer’s Observability feature simplify this process by translating raw 3DS data into actionable insights, helping merchants refine their payment flows and balance security with user experience.

.png)